Children are often told that they can be anything they want to be when they grow up. It’s a lovely idea that is meant to encourage kids to dream big and try new things. But when the time comes to realize those dreams, the tools to discover and realize a satisfying career aren’t always available.

At least that was Kathryn Minshew’s experience.

After receiving her bachelor’s degree in political science and French from Duke University, Minshew began working as a management consultant at McKinsey & Co. But when she began contemplating the next steps in her career path, she struggled to find a resource to guide her.

“I began having these conversations among small groups of close friends, and we came to the realization that there needed to be a resource that addressed millennial needs in particular,” Minshew said. “This group wants and needs something different from the career experience than in years past.”

That frustration led to inspiration and the eventual creation of The Muse, an online career resource that offers a behind-the-scenes look at job opportunities with hundreds of companies, expert career advice and access to personalized career help. Unlike traditional career sites, The Muse creates photo and video profiles of companies that provide in-depth insight into a company’s culture and mission.

“Job hunting is like dating,” Minshew said. “I’m not romantically compatible with every person in the world. In the same way, a single applicant is not compatible with every company. These photos and videos are meant to provide insight into how an applicant will fit in at a company. It’s about more than the ability to perform a job task.”

This focus on culture has made the site wildly popular with millennials, who value culture highly when making career decisions. The company has helped over 50 million people in their job searches and career planning. While that number and the company’s subsequent success is impressive, Minshew, 30, said she is more concerned with the individual lives her efforts are changing.

“Being satisfied with your career path is such a huge part of a person’s life,” Minshew said. “Career is paramount to how people see themselves. I see the job search as a human problem, so it’s exciting to build tools to help people find satisfaction in their lives.”

In many ways, HR is all about politics: balancing expectations, delicately handling a conflict between two parties and knowing when to say the right thing at the right time. Jason Hite knows politics and human resources.

Hite, 37, has an impressive professional track record for a person of any age. Currently the vice president of Xcelerate Solutions, a government counseling organization, he previously worked in the HR department of the U.S. House of Representatives for about 10 years. He started as an HR generalist and worked his way up to director and eventually chief human resources officer. He also served as a key confidant for three successive chief administrative officers at the House.

“One aspect that is hard to balance in the CHRO role, which Jason does extremely well, is the balance between the needs of the organization and that of the employee,” said Tim Blodgett, deputy sergeant of arms at the U.S. House of Representatives, in his recommendation letter. “While in the perfect world those two interests should align, in a practical sense they can be at odds with each other. Jason was able to act effectively on both fronts.”

Hite, whom Blodgett described as the “definition of a consummate professional,” showed impressive HR expertise in the government. Just like he balanced the needs of the individual and the organization, he also was always skilled at balancing his own types of projects. He understood the importance of working in the group setting with stakeholders and at the same time working autonomously on individual initiatives.

One of his many accomplishments was to help the deputy chief administration officer turn around the struggling payroll and benefits team — a problem that needed a speedy resolution.

“Jason worked tirelessly to stabilize the organization and once again proved his value,” said Ali Qureshi, vice president of consulting services at Xcelerate Solutions and former colleague of Hite at the House, in his nomination letter. “His project management skills were put to the test, and Jason led the turnaround, earning the respect of his peers, management and stakeholders on Capitol Hill.”

After Qureshi left the government position to work for Xcelerate Solutions, Hite eventually joined as well. At the government counseling organization, he first made his mark by using his personable approach and analytical acumen to obtain important certifications at a quick and impressive rate.

“I can confidently say,” Qureshi said, “that we have the best human resources executive in the industry.”

Jay Caldwell’s hard work and innovative mind earned him two promotions in only 18 months at ADP. In that time, he supported the move to a pay-for-performance culture, which came from his work in creating ADP’s performance management philosophy, strategy and framework. Other projects include creating a strategic workforce planning discipline; developing a change management strategy and training; a real-time feedback tool and conducting webinars.

Leaders took note. According to Jill Altana, ADP vice president of global talent and development, the CEO of the 55,000-person company noticed Caldwell’s contributions.

“In my entire 30-year career, I have never come across a more talented individual,” she wrote in his application. She added that his innovative thinking, thought leadership and collaboration skills make this 34-year-old a true game changer.

Each month Workforce looks at important stats in the human resources sector. Here are the topics we’re keeping an eye on for August 2016. Comment below or editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

Job candidates, like customers, expect a certain level of service and courtesy when they engage with a company. Yet most companies aren’t even throwing applicants a bone — and that’s not going over well with their talent pool.

A recent study from Future Workplace and CareerArc found nearly 60 percent of job seekers have had a poor candidate experience, and of those 72 percent shared that experience on an employer review site, social networking site or with colleagues and friends. This trend should be concerning to a lot of recruiters.

When candidates post negative reviews for the world to see, it can potentially poison the talent pool, said Dan Schawbel, Future Workplace research director. Today’s job seekers are savvy researchers, reviewing an average of 16 resources when searching for a job, according to CareerBuilder’s 2016 State of Recruitment study. Whether they hear negative reviews from a colleague or read them on Linked In or Glassdoor, it can deter them from applying for a position that may otherwise be a great fit. “Those review can shut off a lot of people who could be good employees,” Schwabel said.

Recruiters may also be surprised to hear what constitutes a negative experience, says Kirsten Davidson, head of employer brand for Glassdoor Inc., the employer review site. It isn’t caused by aggressive interview tactics, or frustrating background check processes. “Most negative reviews come from people who just never heard back,” she said.

And it happens far too often. A whopping 65 percent of job seekers in the Future Workplace survey said they never or rarely receive notice from employers when they submit applications. Similarly, in CareerBuilder’s report job seekers said their biggest frustration is when employers don’t respond to them. “Candidates invest a lot of time preparing an application, yet they feel like the company is investing nothing in response,” Schawbel said. “That sends a bad message about the company.”

Start With a ‘Thank You’

So how do recruiters respond? With many job postings receiving hundreds of applications, there isn’t time for recruiters to send a personal thank you note to everyone who applied. But unless companies have a system in place to at least acknowledge these candidates, employers may be damaging their reputation every time they post an opening.

Even Glassdoor, the company that gives employees a platform to review current and future employers, has struggled to get this one right. A few years ago the site recognized that most of the negative reviews it received were because candidates got no response to their applications.

In response, the company created a checklist of ways to improve the candidate experience, which includes sending some level of response to every candidate who applies. “It was important to find a process that we could scale,” Davidson said. Applicants who are clearly unqualified for the role receive an automated email thanking them for applying and letting them know they are not a good fit but to please stay in touch, while candidates who participate in further screenings and interviews receive more personalized notes with feedback on where they are in the application process and/or why they aren’t right for the job. Since implementing this response process, Glassdoor now has a 73 percent positive interview experience rating compared with the 54 percent average across the entire site.

Taking the time to respond to candidates isn’t just polite; it’s good for the company’s overall image as well, said Robin Richards, CEO of CareerArc. “When you treat candidates well they become net promoters of the brand.” That’s marketing-speak for ‘measuring the loyalty of a firm’s customer relationships.’ When you consider how many people apply for a given job, building loyalty through something as simple as a thank you email can be a powerful marketing tool, he said.

Companies can also use candidate reviews as a way to assess their recruiting process and identify areas that need improvement. And when negative reviews arise, Davidson said she encourages recruiters to respond in a positive and nonconfrontational way. “When you say you are sorry and share what you are doing to improve the process, it can turn a negative experience into a neutral one,” she said. “It also sends a message to the broader talent community that you care about them.” Glassdoor research shows that 62 percent of employees say their perception of a company improves after seeing an employer respond to a review.

Sending thank you notes to unqualified candidates may seem like an added burden in an already time-consuming job, but taking time to acknowledge people who expressed an interest in working for your company just makes good business sense, Richards said. “In a high-tech, high-volume world, a little courtesy makes people feel valued, and that can have a big positive impact on your brand.”

Sarah Fister Gale is a writer based in the Chicago area. Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

Whether you’re just starting your career or have been swimming in the deep waters of office politics for many years, you’re bound to run into some dangerous “fish.”

During my 25-year corporate career I held roles on the front line, in middle management and at the executive level, including a role reporting directly to the company president.

My friends would often ask me if my work environment was political. “It’s like swimming with the sharks.” I would say.

I thought I had come up with a unique — and clever — analogy. I was wrong.

Articles about office politics abound. No wonder in a survey conducted by Robert Half International, 62 percent of the workers interviewed said navigating office politics was at least somewhat necessary to get ahead. So it’s no wonder that a large number of those articles use the swimming with sharks analogy.

In a blog post entitled “Shark Week at Work! Are You Swimming With an Office Shark?” Robert Half, which is one of the world’s largest staffing firms, advises workers to “keep on top of which kinds of sharks are native to your waters so you know what to expect — and how to react.”

So here are the five kinds of shark I encountered during my career and how I survived swimming with them:

The Hammerhead Shark: People who choose less-talented friends over more talented strangers (i.e., you). I am a big believer in mentoring — mentoring others and being mentored. Among the people I established mentoring relationships with were people who were higher up the food chain than I

Those people also served as sponsors. In one instance, an executive wanted to unilaterally hire a candidate. One of my sponsors asked for a competitive process; no guarantees, just a fair shot.

As it turned out, I was selected and the person who expected to get the job ended up working for me. But not for very long: the executive granted her request for a transfer.

The Bull Shark: People who pass on misinformation or rumors about you. In my experience, it was never worth my time to address every rumor or bit of misinformation about me. It was more important for me to build my credibility in individual encounters over time. Thus, some rumors would temporarily take hold. But the reputation I built usually spoke more loudly. “That does not even sound like, Greg” people would say in response to negative rumors.

A case example: I once had to ask for the resignation of a popular employee. Friends of the employee spread the rumor that I terminated him unfairly. Eventually, as people who knew me spoke up, that rumor faded.

The Basking Shark: People who make you look bad so they can look good. The key here is to take the high road. Focus on highlighting your own work. The best response you have to attacks on your work is to produce good work.

Once, after I had completed a temporary assignment, I was told by the regular manager that I had “failed in the field” because an ethics investigation was launched during my assignment (related to conduct that preceded my arrival). However, my response to the misconduct was praised. I never directly addressed the comment. My actions spoke louder than her words.

The Great White: People who highlight your mistakes to higher-ups. When you mess up, fess up. I learned to choose accountability. That is, I didn’t wait until my mistake came to light to reveal it. I always wanted my boss to hear bad things about me from me first. In doing so, I defanged this particular species of shark. As an internal client once said, “Bad news does not get better because it’s older.”

The Sand Shark: People who ask you to support them at the cost of doing what was right. This is a particularly dangerous species of shark, especially if they outrank you. Fortunately, I faced this particular shark only a few times. In each instance, I did what I thought was right and provided a legitimate business explanation about why I chose to carry out an order in a way that was different than directed.

Once I was asked to pay a consultant who was hired to perform ongoing work from a special project budget so that our operating budget would not take the hit. I did find some minimal work on the project and charged just that work to the project budget. I told my boss, that upon closer examination of the invoice, I found that most of the work was part of normal operations and so I charged the work accordingly.

I placed the ball back in the shark’s court (talk about your mixed metaphors!). And the shark acquiesced to how I handled the situation.

In my experience, the primary survival tips in the office shark tank are to do the right things the right way and let your actions, your reputation and your relationships represent you.

So long as we resist the temptation to become one, we can successfully swim with the sharks.

Greg Wallace is CEO of leadership consulting firm The Wallace Group. He is also the author of the book “Transformation: the Power of Leading from Identity.” Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

The Career Hackers is a new blog devoted to helping people start their careers and achieve their goals. Learn more about The Career Hackers on Tumblr.

At SHRM 2016, Workforce Managing Editor James Tehrani spoke with famed zoologist and TV personality Jack Hanna about why he loves HR (it’s the first place he says he goes when he returns to the zoo from a trip), pet insurance, the difficulties of being the source to go to when there’s a tragedy involving animals, how scientists are examining why elephants rarely get cancer and more. Click the video below to watch.

James Tehrani is Workforce’s managing editor. Follow Tehrani on Twitter at @WorkforceJames and like his blog on Facebook at “Whatever Works” blog.

Entering the workforce, whether it be as an intern, part-time worker or full-time employee, is both an exciting and daunting challenge. It requires countless hours being devoted to researching job openings, creating résumés and cover letters, preparing for interviews and, hopefully, receiving and deciding between job offers.

Once a job seeker accepts a job offer, one of two fates is likely to unfold:

The first, a positive experience full of one-of-a-kind learning opportunities that are both fun and educational and take place alongside intelligent, friendly and supportive co-workers who will serve as possible connections and resources throughout the newbie’s future career.

Moritz Kothe, kununu

The second, an utter disaster full of boring tasks and surprise responsibilities, resulting from poorly skilled employers, negative work environments, and misleading HR professionals who misrepresented the company during the interview process.

This second fate is what Moritz Kothe, CEO of kununu, an employee rating site new to the U.S. market via a partnership with Monster, describes as the “Oh my God, what have I done?” feeling that job seekers experience all too often after accepting a job offer.

In a kununu survey, which sampled 1,019 employed Americans 18 and older, it found that 23 percent of participants reported having been misled during a job interview, which is almost the same amount of people who reported having been misled on a first date. Furthermore, 3 out of 10 job seekers felt it is often difficult to receive accurate, honest information about the day-to-day experience of a specific job during the interview process.

Based on these findings, it is no wonder that many Americans regret a job after accepting an offer. Fortunately, this does not have to be the case for everyone. The solution here is research. And lots of it.

Job seeking Americans are curious about many aspects of their potential future employer. For example, Kothe says, “some might be interested in what opportunity advancement is like, and some might be interested in what the culture’s like.” Kununu and other employment rating platforms allow inquiring job seekers to access the answers to these questions as told by real employees who have shared their thoughts, experiences and ratings. This allows interested candidates to receive accurate job and company descriptions from people who have actually experienced it firsthand.

Besides using such platforms as kununu or Glassdoor, job seekers should do as much background research on a company as possible by thoroughly examining the company’s websites, press releases, mentions in the media, etc. They should also seek out any possible connections they might have to a current or past employee of a company, because a job seeker can never have too much information when it comes to choosing which company is the right fit for them.

Whether it be through employee review platforms, internet research, or speaking to personal connections, conducting thorough research about a potential employer is vital. This is the key to finding an internship, part-time job, or career that makes a person happy and helps prepare them for success in future aspirations.

AnnMarie Kuzel is a Workforce editorial intern. Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

The Career Hackers is a new blog devoted to helping people start their careers and achieve their goals. Learn more about The Career Hackers on Tumblr.

Workplace deaths and injuries are on the rise, having reached their highest levels since 2008, despite dramatic improvements in worker-safety practices over the past few decades.

According to a recent study by the National Safety Council, a nonprofit organization that promotes health and safety, 4,132 workers died of unintentional injuries in the workplace in 2014, up 6 percent from the previous year, reflecting the largest spike in 20 years, according to safety expert John Dony.

“Forty years ago, we had lots of people dying from doing very dangerous work, but we realized that we need to put people in harnesses when they’re working on tall buildings, and we need to develop a system for reporting accidents,” said Dony, director of the Campbell Institute, the research arm of the National Safety Council. “We still have a good story to tell around workplace safety in the United States, but the fact that we’ve had a long history of maturity and improvement and yet we are seeing an increase in deaths and injuries is troubling.”

According to the council’s report, which is based on federal data, certain industries have seen a sharper rise in unintentional injuries such as falls, motor vehicle accidents, machinery accidents and exposure to harmful substances.

For employers, this can mean higher workers’ compensation costs and more indirect consequences like lost productivity, higher training costs to replace injured workers, lower employee morale and greater absenteeism. According to a 2016 study by the Liberty Mutual Research Institute for Safety, U.S. businesses spend about $1 billion a week in workers’ compensation costs for the worst occupational injuries. These include overexertion because of lifting, pulling or throwing, falling, being struck by an object and roadway accidents.

Older workers are being killed or injured in greater numbers.

According to the U.S. Bureau of Labor Statistics, there were 1,691 fatalities among workers 55 and older — a 4 percent increase over 2013. A recent report by Washington state’s department of labor found that more than half of workplace deaths in 2015 involved people over 50.

An aging workforce is likely one factor contributing to the increase in workplace deaths and injuries, Dony said, adding that it’s not clear if physical limitations associated with aging are to blame.

Whatever the reasons, employers need to do a better job of making their workplaces safer, he said.

Rita Pyrillis is a writer based in the Chicago area. Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

Our retirement is not our parents’ retirement. For many American employees in their generation, a good job meant access to a secure retirement income they could not outlive. Employers took center stage, assuming most of the financial risk of funding that retirement with employees largely removed from the process. Today, employers are far more likely to be facilitators of retirement saving, playing a critical supporting role while the employee is the star planner of the retirement show.

How did the idea that employers should offer secure retirement benefits through defined benefit plans, or pensions, evolve? How and why did this change over time to put more of the responsibility on employees to save through defined contribution plans such as 401(k)s? And how can benefits managers use new savings tools and employee benefits available today to help their employees retire smarter, happier and more financially secure?

The U.S. Retirement System

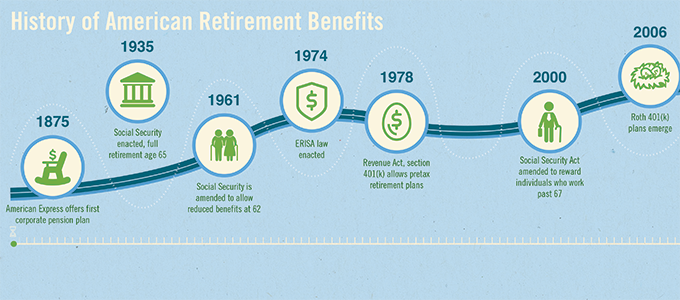

Retirement is a fairly modern concept with origins in military history. Until the late 1800s, those who had to work to earn their living worked their entire lives. Historians credit the Roman Empire with conceiving the idea of an income that continued after work service by offering pensions to retiring soldiers during the first century B.C. While this initiated a long tradition of military pensions, the concept of ceasing to work in later life didn’t begin to spread to the rest of the workforce until the 19th century.

Today, we think of a pension as a series of payments to be made to workers after the end of their working years. In the United States during the mid-1800s, a “pension” also referred to disability and survivor benefits. During the middle of that century, larger cities began to offer disability and retirement income benefits to police and firefighters. This trend expanded over time among public sector workers.

In 1875, The American Express Co. created the first private pension plan in the U.S. for the elderly and workers with disabilities. According to the Pension Research Council, by 1926 approximately 200 private pensions had been established by larger employers in the United States. Early pension benefits were designed to pay out a relatively low percentage of the employee’s pay at retirement and were not designed to replace the employee’s full final income.

The idea that employees should have some kind of a defined benefit in retirement gained traction during the boom decades that followed World War II. Large corporate employers took a paternal approach to their workers and offered pensions as part of their talent recruitment and retention efforts.

And it worked. It was not uncommon for workers to spend their entire careers at the same company back then. Compare that to 2014 when the U.S. Bureau of Labor Statistics reported the average employee tenure was 4.6 years.

Benefits grew richer over time, with many pension plans offering replacement incomes that covered more of the employees’ average pay. By 1970, 26.3 million private sector workers (45 percent of all private sector employees) were covered by some kind of pension plan. Participation held steady for several decades with 43 percent of private sector employees still covered by 1990.

With a traditional defined benefit plan, employees had little direct control over their retirement. To earn higher lifetime benefits in the plan, they could work longer, make a higher salary or live longer — but the employer controlled the contribution formula and the investments, and generally made all the contributions to fund the plan.

The ’70s brought America staggering inflation, disco, and legislation that changed retirement forever. In 1978, Congress passed The Revenue Act of 1978 in which Section 401(k) cleared the way for the establishment of defined contribution plans. The idea was revolutionary: Employees would be able to contribute their own money in a tax-advantaged way to an account to supplement any other retirement benefits they had with tax incentives for the employer to also contribute. The upshot? Over the past 38 years for the typical U.S. employee, the responsibility for developing a sustainable retirement income has shifted from the employer to the individual.

A “defined contribution plan” takes its name from the ability of the employee and/or employer to contribute a fixed sum to the plan. Over time, different types of plans evolved to serve different types of employees: 401(k) plans for private sector employees, 403(b) plans for nonprofit and public education employees, 457 plans for state and municipal employees and the Thrift Savings Plan for federal employees.

Today, the traditional pension is an endangered species. For the past decade, employers have been terminating defined benefit plans in record numbers and moving toward defined contribution plans. According to the Employee Benefits Research Institute, by 2011 69 percent of employee participants in a retirement plan at work were participating in a defined contribution plan, 24 percent were participating in both a defined contribution and a defined benefit plan, and just 7 percent were in a defined benefit plan only.

Sources: NelsonHall; 2015-16 HR Systems Survey, Sierra-Cedar; National Association of Professional Employer Organizations. Graphic courtesy of Financial Finesse.

Employees are Unprepared or Underprepared for Retirement

Employees are largely unprepared to shoulder the risk of saving adequately to fund retirement and making wise investment choices with those savings. According to the Financial Finesse 2015 Year in Review research on employee financial trends, only 22 percent of employees are confident that they are on track for retirement, even though 84 percent contribute to their retirement plan. (Editor’s note: The author is the CEO of Financial Finesse.)

When it comes to choosing appropriate investments in their retirement accounts, employees are also falling short. Only 46 percent of male employees and 36 percent of female employees are confident their investments are allocated appropriately in their retirement accounts. Problems with cash flow management and debt have a cascading effect on suppressing retirement savings rates.

Recent enhancements in retirement plan design, such as auto-enrollment and auto-escalation, are not enough to increase preparation. Employers must address cash management and overall financial wellness, educating them to better understand their role in retirement preparation and freeing up more funds for contributions toward their retirement goals. Integrating plan design enhancements with employee benefits education and communication can improve retirement preparedness.

Employers can increase the likelihood that employees will be better prepared for retirement by integrating retirement education into an overall financial wellness program that looks at cash flow, employee benefits and long-term financial goals. When in place, Financial Finesse’s research shows repeat users of workplace financial wellness benefits have shown a 88 percent improvement in the percentage of workers who are on track for retirement. Forward-thinking employers can take these six steps to improve employee retirement preparedness:

Increase the default deferral rate.

Automatically enroll employees in auto-escalation of their retirement savings.

Implement re-enrollment in the plan’s qualified default investment alternative, also known as a QDIA, an investment that may be used by retirement plan sponsors in the absence of direction from the plan participant.

Offer benefits planning to help employers understand and maximize the value of their benefits.

Enhance employee communications.

Develop a comprehensive financial wellness program.

More — and More Complex Benefits Choices

Employers and employees are also navigating major changes in health insurance benefits, including the move to high deductible health plans in conjunction with health savings accounts, which were created in 2003. Employees in general do not yet fully understand the advantages of HSAs in preparing for retirement, and employers have a high hurdle in helping them maximize this benefit.

Additionally, since the Roth individual retirement account was introduced in legislation sponsored by the late-Sen. William Roth Jr., R-Delaware, in 1997, Americans within certain income limits have been able to save after-tax contributions in an account that grows tax-free for retirement. The Roth 401(k), allowed by legislation passed in 2001, gave those employers who sponsor retirement plans the option to offer employees after-tax/tax-free distributions within the 401(k) structure. While slow to gain adoption, recently employees have been choosing Roth options in greater numbers.

Healthy Confusion

Employees generally remain confused over which health insurance and retirement plan options are best for their situation. They look to their employers to offer guidance on how to choose what’s right for them. Employers may consider offering targeted educational workshops or webcasts, print or email communications and personal financial coaching to help employees understand and maximize these benefits.

For health care, this includes ways to review the health coverage and out-of-pocket costs they have today, understand and compare plan options, decide which option is best for their unique situation and prepare for changes they’ll need to make in their cash management to take full advantage of the value of an HSA. Employers can also offer workers retirement plan education on the differences between pretax and after-tax contributions, and the general types of situations where one or the other makes sense.

The good news is that employers are well-positioned to help employees be the star planner of the retirement show so they can meet the challenges of improving retirement preparedness and make wise benefits decisions. According to a TIAA survey, 81 percent of respondents said they trust financial information from their employer. Financial Finesse’s 2015 Retirement Preparedness Research shows that the number of employees who say they are on track for retirement doubled with repeat usage of workplace financial wellness programs. While technology such as online financial education can play a supporting role, employers will gain the most influence and employee satisfaction with offering interaction with a financial coach who can help employees through the decision-making process.

Employers who offer support, guidance and education to assist employees in taking center stage throughout their careers in order to retire comfortably will have loyal, more financially confident employees. As reporter Emily Brandon said in “Pensionless: The 10-Step Solution for a Stress Free Retirement,” “Although you may never receive a pension from a former employer, you can do a lot to make the most of the retirement benefits you do have.”

With employers leading the way in prepping workers for the future, 21st century employees can still have a comfortable, secure retirement.

After receiving her bachelor’s degree in political science and French from Duke University, Minshew began working as a management consultant at McKinsey & Co. But when she began contemplating the next steps in her career path, she struggled to find a resource to guide her.

After receiving her bachelor’s degree in political science and French from Duke University, Minshew began working as a management consultant at McKinsey & Co. But when she began contemplating the next steps in her career path, she struggled to find a resource to guide her. “Job hunting is like dating,” Minshew said. “I’m not romantically compatible with every person in the world. In the same way, a single applicant is not compatible with every company. These photos and videos are meant to provide insight into how an applicant will fit in at a company. It’s about more than the ability to perform a job task.”

“Job hunting is like dating,” Minshew said. “I’m not romantically compatible with every person in the world. In the same way, a single applicant is not compatible with every company. These photos and videos are meant to provide insight into how an applicant will fit in at a company. It’s about more than the ability to perform a job task.”