Becky Beach admits she doesn’t know much about Social Security, but she definitely thinks it won’t be around when she needs it. That’s why the 40-year-old lifestyle blogger plans to start taking the benefit when she turns 62.

“I plan to take it out as early as I can,” Beach said from her home in Arlington, Texas. “I don’t really know that much about Social Security, but I hear it’s going to go away.”

Lots of people like Beach think similarly. In fact, only 4 percent of retirees wait until the optimal age of 70 to take their Social Security benefit, a new study by robo-adviser United Income said. Retirees lose out on $3.4 trillion in possible income, which on average is $111,000 per household, because they don’t take Social Security at the best point in their lifetime.

“Most people don’t claim Social Security at the optimal age from a financial perspective because they may not be having the necessary retirement planning discussions,” said Jason Fichtner, former chief economist at the Social Security Administration, and co-author of the study. “Financial advisers, employer HR departments and policymakers could do a better job with educational materials and encouraging people to spend more time sorting through this important decision.”

Social Security provides more than $1 trillion in benefits to 64 million Americans.

Nearly all (92 percent) of retirees that took Social Security at the wrong time would have seen their income increase had they pinpointed the right time. In fact, more than half of these retirees could have increased their income by more than 25 percent in their 70s and 80s, the report said. That’s usually when people see spikes in health care costs.

Today, Social Security provides more than $1 trillion in benefits to 64 million Americans. It represents a third of retirement income for seniors, which averages $1,461 each month.

There is no doubt the system is being stressed with increased life expectancies, but the doomsday scenario of the system going broke isn’t exactly right, Fichtner said. The latest Social Security Administration report shows that the trust fund reserves are expected to be used up (if nothing is done) by 2035. If Congress chooses to do nothing to fund Social Security, it will still be able to pay out 80 percent of what working Americans are owed after 2035.

“The trust fund may become depleted, but once depleted, it will pay out what it collects,” Fichtner said. “By law, Social Security will pay out 80 percent of what is promised.”

The study showed that most people should wait until 70 to claim their Social Security benefit. While workers can start claiming their benefit at 62, the amount increases on average about 8 percent each year they delay the claim. The Social Security Administration reported a 62-year-old would receive a $725 monthly benefit if they claimed today. Choosing to delay the benefit until age 70 would increase the amount to $1,280, a 177 percent increase.

While waiting to get a bigger paycheck sounds great, it may not always be feasible, said Colleen Jaconetti, senior investment analyst at The Vanguard Group. It’s not wise to completely deplete an investment portfolio to accomplish this, she said. In addition, some people may not be able to work or earn enough money in their later years to get them to 70.

“A lot of people don’t realize that they need to figure out how they fill that gap” between 62 and 70, Jaconetti said. “It’s a complicated problem.”

Jaconetti pointed out that those who are able to bridge the gap and delay claiming Social Security can also see other benefits from their decision. Some may see a lower tax bill while in retirement because Social Security taxes may only come from 85 percent to 50 percent of that income. In addition, relying more on Social Security in later years may allow heirs to inherit unused assets from retirement accounts. The important thing, she said, is that people make informed decisions on their health, financial status and other factors to determine the right time to claim the benefit.

Fichtner and Jaconetti agreed that most people are like Beach, they really don’t think about Social Security and may only have time to hear or see the headlines. It would be helpful for human resources leaders and policymakers to help people understand the options well before it becomes their time to make this often permanent decision to claim Social Security benefits. The study looked at Social Security messaging and suggested that the Social Security Administration revisit how it describes claiming age. Currently, age 62 is labeled “early eligibility age.” Fichtner suggested age 62 could simply be labeled “minimum benefit age” while age 70 could be labeled the “maximum benefit age.”

“How we talk about this can change behavior,” Fichtner said. “The little things can make a difference.”

At a time when careers in government are increasingly underscored with public and political pressure, Kirsten Wyatt is sounding the alarm about the public sector workforce.

“The government needs to wake up and realize there’s a talent war,” said Wyatt, executive director of the Oregon-based Engaging Local Government Leaders, a nonprofit promoting diversity, education and networking among local government employees on a national level. “If you’re going to be competing for entry-level or jobs you want to fill with talent you can then nurture, you need to put in more effort.”

Public sector agencies from the massive federal government to tiny rural townships face unique challenges when competing with private businesses for talent. Recruiting and retention is a recurring concern for the skill set often associated with public service employees. And it’s no secret that private sector companies typically offer substantially higher wages and more flexible work schedules. And there are other factors coming into play.

Prime among them is the so-called silver tsunami, a wave of baby boomers exiting the workforce into retirement. Studies show some 10,000 boomers retire every day, leaving a huge gap for public sector employers to fill.

According to the U.S. Office of Personnel Management, the average age of a full-time federal employee is 47.5 years, with 45 percent of the workforce over 50 years old.

The Congressional Research Service indicates 52 percent of public workers are age 45 to 64 compared to 42.4 percent in the private sector.

Federal workers are older than state and local government employees, too, studies show. Of those age 45 to 64, 56.7 percent are federal, 52.1 percent are local, and 49.7 percent are state employees.

In a 2018 survey by the Center for State & Local Government Excellence, public sector HR directors report higher numbers of retirements in 2018 over 2017.

Another challenge: Public agencies depend on tax base or bond-measure revenues to create new jobs and rehire for open positions. Hiring freezes are not uncommon even in flush economic times.

Nannina Angioni

“When taxpayer dollars are on the line, protections and processes come into play that an untrained, private sector employee would not even consider,” said Nannina Angioni, a labor and employment attorney and partner of the Los Angeles-based law firm Kaedian LLP.

Angioni said it can be costly and time consuming to find employees with public sector experience for entry-level positions given the increased ethical considerations, regulatory issues and legal obligations that typically don’t apply to private sector workers.

Still another challenge: enticing people to technology jobs. While millennials exhibit technological advantages being digital natives, it’s also one reason they are scarce in government workplaces with antiquated systems where they can’t sharpen their skills, said Kris Tremaine, a senior vice president focusing on the federal public sector at ICF, a global consulting and technology services company.

Although millennials will comprise 75 percent of the workforce by 2025, they currently make up only 10 percent of the federal sector technology workforce, said Tremaine.

Kris Tremaine

Eighty-two percent of the Center for State & Local Government Excellence’s survey respondents indicated recruitment and retention as a workforce priority. They’re finding it difficult to fill positions in policing, engineering, network administration, emergency dispatch, accounting, skilled trades and information technology.

“When it comes to recruiting talent, you need to go where the talent is,” said ELGL’s Wyatt, adding that while many public sector HR departments continue to advertise jobs in newspapers, potential talent is hanging out on social media.

While Wyatt calls many job ads “boring,” she also notes successful efforts such as one produced by the city of Los Angeles for a graphic designer. The ad appeared as if a child drew it with a crayon. It went viral.

Fort Lauderdale, Florida, human resources professional Jody Blake posts jobs on social media featuring eye-catching images of palm tree-lined beaches or building plans.

To fill vacancies in Fort Lauderdale’s 2,500-member workforce, Blake uses Twitter, Facebook, LinkedIn, ZipRecruiter and Indeed.

She’s had the most success with LinkedIn, especially for stormwater and wastewater engineers. She posts jobs on engineering group sites at no cost and uses LinkedIn’s Recruiter Lite program to maximize her efforts.

“I believe in getting the word out any way you can,” she said. “Even if people aren’t interested themselves, they may know someone who is.”

The public sector should take a page from the private sector in hiring practices, including internships, career fairs, meet-ups, events, social activities and using more technology, said Tremaine. Blake, meanwhile, also seeks people with a passion to make a difference. Jobs emphasizing social good attract millennials who want to be part of making a difference “such as in helping Americans stop taking opioids or climate change issues,” Tremaine added.

Wyatt said, “You can work in sustainability, be a librarian, police officer or an engineer and all work for a local government with that public service ethos at the core of your job every day.”

Millennials Embrace Collaboration

Human-centered open plan designs supporting teamwork where employees of different skill sets gather is important, said Tremaine.

While millennials skip from job to job often for higher pay, “some want clearer paths to growth and an understanding of where they fit in the organization,” Tremaine said, adding they prefer a coaching-mentor relationship to a boss.

Streamlining onerous paperwork and a protracted timeline involved in public sector employment may attract more employees, Tremaine said.

So too would the ability to leave a job and return “and not lose all of your benefits while drawing private sector best practices into the government,” she added.

Jody Blake

Fort Lauderdale attracts many people looking for a switch after many years working in the private sector. While they made more money in private industry, they seek the security of the public sector, Blake said.

The city of Weston, Florida, took a different approach 21 years ago by outsourcing most positions per its charter.

“Probably 70 percent or more of a government budget is the cost is to pay employees,” said City Manager John Flint.

Only 10 positions for the city of Weston are in-house: six department directors, a city manager, two assistants and a clerk. An assistant city manager handles necessary HR functions such as insurance and payroll contributions.

Law enforcement is provided through the Broward County Sheriff’s Department. Other city jobs are filled by government outsourcing services such as C.A.P. Government, Calvin, Giordano & Associates, Municipal Technologies, and Weiss, Serota, Helfman, Cole & Bierman.

“All of the people here are by invitation and not by right. If the people assigned to us don’t meet our expectations, it is easier for us to replace them. I don’t have to spend my time managing people. I can manage the city and spend more time with our elected officials and residents,” said Flint, adding Weston’s approach offers greater flexibility and efficiency.

Some outsourced employees have been with the city before its incorporation in 1996 when it was a community development district, said Flint. When the city changes service providers (which hasn’t happened in a decade), Flint ensures the incoming provider retains the current employees and keeps their salaries and benefits at least equal to the previous provider.

Kaedian LLP’s Angioni said that once they are hired, many public sector employees stay in their job for decades for the perks of consistent work hours, minimal demands outside of their set schedules, union benefits, rights to reinstatement, pensions and appeal rights to disciplinary actions.

Career Moves

The public sector also offers the ability to try different careers while retaining benefits in one organization.

An agency might consider moving someone who’s been an analyst in community development for a few years into public utilities for another few years to increase their knowledge base and broaden their skills.

Such moves keep employees “engaged, excited and continually learning” while also giving departments “a fresh set of eyes,” Wyatt said. That’s important to retention, given the hundreds of thousands of dollars spent on employee wages, benefits, training and development over a five-year span, she added.

John Flint

To retain employees in one of the most difficult public sector jobs — solid waste collection — Greenville, South Carolina, Solid Waste and Recycling Manager Mildred Lee treats a crew to lunch monthly to show her appreciation and elicit their input.

She’s retained employees by leading an effort to convert solid waste collection from five to four days. A supervisory mentoring program for all frontline solid waste employees has transitioned two into management.

A 2018 survey by the Center for State & Local Government Excellence noted that more than 45 percent of the respondents offer flexible scheduling, 65 percent support employee development and training reimbursement, 37 percent host wellness programs or on-site fitness facilities, and 34 percent provide some form of paid family leave.

Wyatt said she receives increasing feedback about the value the midprofessional generation places on paid family leave.

Kansas City, Missouri, recently finished a one-year paid family leave pilot program. It was utilized primarily by male police officers. It’s the hardest job for which to recruit and is typically dominated by young men, said Wyatt.

“You look at the long-term impact that has on employee morale and loyalty and who you choose to work for with everything else being equal,” she added.

As the public sector starts to see the dismantling of retiree benefits, one useful tool may be adopting the Individual Medicare Marketplace for retiree health care programs, “a model generally far more affordable for retirees while offering cost savings for employers,” says Marianne Steger, director of public sector strategy at Willis Towers Watson and former health care director for the Ohio Public Employees Retirement System.

Retaining employees has meant offering low-priced health insurance, a generous retirement plan, educational incentives, annual reviews typically with pay increases and the ability to start off at a good rate of vacation time accrual, said Fort Lauderdale’s Blake.

Blake offers advice to new hires on how to improve their profile to increase their promotion chances. Employees are surveyed on the work culture. Employees are called community builders while residents are called neighbors.

Wyatt and her husband Kent — both former public sector employees — founded ELGL after noticing local government education, training and networking was siloed based on job title. Its 4,000 members nationwide represent a cross-section of entry-level employees to mayors and city managers.

“It helps when librarians can learn from planners and cops can learn from finance directors,” said Wyatt.

Their organization provides collaboration and cross-departmental training through a technology network connecting public sector employees in one part of the country to others elsewhere to help deal with problems for which others have found solutions.

It also provides online content, monthly webinars, regional pop-up conferences and a national conference. Informal meet-ups are held on college campuses to introduce local government careers to college students.

Further, it focuses on increasing the number of women and people of color into local government leadership to reflect U.S. community demographics.

While there is much focus on age demographics in public service, Wyatt said what most people in a public service career want is no different than anyone else: “feeling recognized for a job well done, independence and learning something that takes them to the next step in their career.”

Wyatt has seen some members go through a career crisis as they contemplate a move to the private sector for more pay and better fringe benefits.

“They choose to stick with government,” she said. “They built a network that supports them and reminds them it’s work worth doing and that’s powerful.”

Providing such care while working a full-time job is both physically and mentally taxing for most employees, and studies even show that burnout from caregiving responsibilities cost companies nearly $13.4 billion each year in health care expenses.

Backup elder care is a benefit some organizations are considering for employees. In general, there are two primary types of elder care benefits:

Dependent care assistance plans. These plans deduct a certain portion of an employee’s paycheck (gross amount before taxes) to pay for elder care costs. According to Forbes, currently, 41 percent of employers offer this benefit.

Respite care. Offered by only 7 percent of companies, this benefit offers short-term care to family members when an employee needs to rest, take time off or go into work.

Flexible work options. These options include allowing caregiver employees to work from home, have flexible hours during the day, or providing paid time off.

Care subsidies. This benefit would help employees with the cost of elder care with subsidies covering either direct costs or backup care.

Support groups. Employers can create onsite caregiver support groups for employees. This will allow them to speak with fellow coworkers dealing with caregiving of senior parents and perhaps find some value in communicating. The employer may also provide online support group resources if onsite isn’t an option.

Respite care is the benefit most commonly referred to as backup elder care, and it is provided through the private insurance companies employers contract with. It is a voluntary benefit, so employees who do not need backup elder care do not have to enroll. If an employee does not know whether they have these benefits, they should speak with a human resources or benefits manager.

The Professional Impact of an Aging Population

According to the U.S. census, nearly 70 million Americans will be over the age of 65 by 2030. This may sound like a shocking statistic to many, but as the baby boomer population ages and exits the workforce, their children and younger relatives might be required to act as caregivers in many situations.

Backup elder care benefits helps employers reduce the amount of stress caregiving employees experience by allowing them to know that their loved ones will be cared for while they are at work.

Studies show that employees prefer to work for companies that offer a reasonable work-life balance. Companies should keep this in mind when deciding whether to provide backup elder care. Caregiving can be exhausting, even for the most dedicated individual and when paired with a demanding work schedule, employees become overwhelmed.

By providing elder care, caregiving employees will have more flexibility. This means limiting the choice of missing a workday or taking care of an infirm parent.

Scheduling Flexibility

According to a 2012 CareerBuilder study, nearly 40 percent of employees who voluntarily left the workplace did so because of a poor work-life balance. Few employees appreciate being called in at the last minute to work abnormal hours, but sometimes it is unavoidable. Most managers and supervisors are aware of this, but if their employees have outside caregiving obligations, they simply will not be able to depend on them to work outside of normal work hours.

Many employees also have difficulty balancing their caregiving responsibilities with regular work hours. Caregivers are more likely than other employees to leave work early and use paid time off to look after loved ones.

This can place a strain on the workplace when a valuable employee is not able to work their normal hours, especially if other workers are forced to pull their weight for them.

Millennials make up 35 percent of the American workforce, and as members of the baby boomer generation age millennials will have to accept the role of family caregiver. As of 2013, nearly 19 percent of caregiving employees were under the age of 40, and this percentage is only expected to increase in coming years. If a company fails to keep such statistics in mind when recruiting younger professionals, it may start to notice its talent pool shrinking because of its perceived lack of concern for its employees who double as caregivers.

Offering Backup Elder Care

As time continues to prove backup elder care should be a benefit offered by an employer, more companies are taking responsibility in offering these benefits. A main provider of backup elder care is Bright Horizons. They offer 24/7 backup elder care to employers. The organization is understanding of both the employer and employee’s needs and even provides an online self-service support for if the employee wants to choose and hire the caregivers themselves. Other providers include Care.com, LifeCare and Town + Country Resources.

Prices vary per provider, with some backup benefit providers estimating a minimum of $15,000 per year to be paid by the employer. The average amount of an employee paying for elder care services is estimated at $4 to $6 per day if the employer subsidizes the cost.

Offering backup elder care is not only beneficial for employees and their loved ones but a company’s bottom line as well. Caregiving employees cost companies millions of dollars in lost hours each year, and by offering backup elder care, you may be able to make up for these losses and retain your most valuable employees who want to work for a company that understands their needs and the importance of family.

Target-date funds had been in the 401(k) lineup for more than a decade at Zurich American Insurance Co., but it wasn’t until 2014 that the company started using the investment to automatically enroll workers.

One reason target-date funds have become popular?: Costs have come down considerably over the past few years and are certainly well below what it would cost to have all these investments managed individually.

After doing an evaluation at that time, target-date funds were the best option for the company to automatically put workers into a professionally managed investment account at a reasonable and low cost, said Dawn Carthan, benefits consultant at Zurich.

“Target-date funds went hand-in-hand with auto-enrollment,” Carthan said.

Today, the commercial insurer’s reasoning is similar to many companies using target-date funds when automatically enrolling workers into 401(k) plans. In its “How America Saves 2018” report, investment management giant Vanguard found that 51 percent of participants were invested in a target-date fund. For plans automatically enrolling participants, 96 percent were enrolled directly into a target-date fund.

Because of the rapid growth of target-date funds, Vanguard expects 70 percent of participants will be invested in them by 2022.

At Zurich, 94 percent of plan participants are using target-date funds, with 68 percent invested entirely in one. That second number is largely because of a re-enrollment project that took place in the first quarter this year. Prior to the initiative, less than half of participants were invested entirely in one target-date fund, a Zurich spokeswoman said.

“Target-date funds have definitely taken off,” said Jean Young, author of the Vanguard report and senior research analyst for the Vanguard Center for Investor Research. “These professionally managed options are so much easier today.”

Young said target-date funds are popular for three reasons: first, they are professionally managed investments that start at a higher rate of risk when a participant is younger, and continually rebalance, moving to a more conservative asset allocation as that person reaches retirement age. Second, costs have come down considerably over the past few years and are certainly well below what it would cost to have all these investments managed individually.

Finally, the Pension Protection Act of 2006 allowed plan sponsors to automatically enroll workers into what is called a qualified default investment alternative, or QDIA, a type of investment that would meet a participant’s retirement needs. Target-date funds fall under that umbrella.

The QDIA qualification catapulted target-date fund growth. Last year, target-date mutual funds pushed over the $1 trillion mark compared to $158 billion in 2008, according to Morningstar’s Target-Date Fund Landscape Report. Net inflows surged to $70 billion in 2017, compared to the $40 billion in net flows every year since 2008.

Three providers, Vanguard, Fidelity and T. Rowe Price, have dominated the field, holding a combined $774.6 billion in total assets in 2017. Within the space, 95 percent of all inflows last year built on the longstanding trend in going to low-cost funds. The average expense ratio for target-date funds was 0.66 percent in 2017, compared to 1.03 in 2009.

Low cost doesn’t necessarily mean best fit, said Jeff Holt, director of multi-asset and alternative strategies for Morningstar Research Services.

“There has been this huge move to low cost,” Holt said in a recent webinar. “But plan sponsors and investors should be aware that it’s not a guarantee that they are going to get the better results despite having the fee advantage.”

Plan sponsors should be wary of having a false sense of security with this QDIA, said Ron Surz, president of Target Date Solutions, an investment management firm based in San Clemente, California.

Surz said many plan sponsors offering target-date funds assume that any available ones will work as the QDIA for their 401(k) plan. Plan sponsors often choose funds out of convenience for themselves rather than the best fit for participants, Surz said.

It’s no coincidence, he added, that two of the three largest target-date fund providers are also the largest record keepers in the retirement benefits industry.

“Many plan sponsors think they are safe,” Surz said. “As fiduciaries, they need to be aware of their duty of care to find the best target-date fund for the beneficiaries and not the most convenient one.”

Getting together with old high school chums, not surprisingly, can be an eye-opening experience.

There’s bigger guts, less hair and a divorce rate approaching Tom Brady’s lifetime passer rating. There’s also bragging on our overachieving children and woebegone tales of trips in our youth that never should have happened. “How did we ever survive high school?” is an all-too-common refrain as these stories unfold, followed by a long pause, a collective shaking of heads and, “OK, who needs another beer?”

For the most part I was prepared for all of that. But no 20-pound fish tale or boastful memory of eighth-grade on-court hoops supremacy could have prepped me for a question that hit me from the blind side not once, not twice, but five times in one afternoon.

“Are you retired yet?”

Me (somewhat befuddled): “Umm, well, no … no, I’m not,” I sputtered after the initial query. By the third round of questioning I had abandoned the “Umm, well” and the “no, I’m not” for a much more direct, succinct, “No.”

I guess I shouldn’t have been shocked at the question. Early retirement is not some new concept created by Silicon Valley entrepreneurs. My dad retired as a union plumber in his mid-50s and spent his encore career as the World’s Greatest Grandfather. Heck, Andre Ethier is 35 and officially retired in August after making $115 million over 12 seasons playing for the Los Angeles Dodgers.

It’s just one of those age-appropriate questions that I should have expected to hear. Sort of like when you’re 18 and it’s “you don’t have a fake ID yet?” or at 40 and, “Viagra or Cialis?”

Considering that most of those friends are retired now, I admit to a little pang of jealousy. They may or may not have a daily routine; they work on their boats and kayak on their local lake whenever they feel like it, and they hit up day baseball games. Like, why them and not me?

Well … most of them entered the trades straight out of high school, joined a union, got really good at their jobs and could retire after 30 or 40 years with a pension.

I chose to put my hands on a keyboard instead of a wrench and got into journalism. No pension. No boat. No weekday baseball games. However, I am part of a profession whose members are considered enemies of the state, according to our president. So I have that going for me.

And no retirement yet.

For my friends, their retirement from the daily workforce did not come without sacrifice. Bitterly cold winters on a construction site, scorching summers toiling over freshly laid asphalt and hopping in and out of delivery trucks schlepping barrels of beer or 60-pound freight packages takes a physical toll.

But a trustworthy employer and a strong union assured their retirement — and my dad’s and Andre Ethier’s, for that matter — at a relatively young age.

I have a feeling they are among the fortunate ones — or at least they are smarter than the average enemy of the state. As traditional employer-funded pensions fizzle and employees take greater responsibility for funding their retirement, a recent study from the Consumer Bankruptcy Project reveals that people 65 and older are filing for bankruptcy three times more than the rate in 1991.

A shrinking social safety net combined with longer waits to maximize Social Security benefits, pensions being replaced by 401(k) plans and ever-increasing health costs are driving this spike in bankruptcies, the study suggests.

What can U.S. organizations do to help stem this alarming trend? Frankly, we can’t expect companies to foot more of the direct costs of retirement — in other words, re-instituting pensions — just for altruistic reasons.

Generation X will likely rely on today’s model of a defined contribution plan as the bulk of their retirement planning. But what awaits Gen Y and Z?

Is there a fresher, more innovative solution than what we have today — a 401(k) with a financial well-being service tacked on? We live in a hyperdisruptive economy crying out for retirement reform that cuts across political partisanship.

Business leaders can step up, too, not necessarily tapping their coffers but opening their mouths and minds to help solve the pending retirement crisis.

I am truly happy for my retired friends as they pursue their personal passions. They worked decades to achieve it. There are many with meaningful jobs at 65, but others — those stuck in the work-to-live category — deserve a shot to get out on a lake after years of toiling away, too.

Because really, wouldn’t you prefer the option of sitting in a kayak on some serene lake versus sitting behind a desk when you’re 65?

Rick Bell is Workforce’s editorial director. Comment below or email editors@workforce.com.

The Bureau of Labor Statistics reports that today’s mobile workforce is changing jobs nearly a dozen times.

For 35- to 44-year-olds, a little over a third take jobs that last less than a year. It doesn’t allow for a lot of time to sock away money in a 401(k) account and as a result, many workers are cashing out what little they have.

It’s a serious problem because too often people don’t realize the whopping penalties or the consequences they face when wiping out retirement savings, said Spencer Williams, president and CEO of financial consulting group Retirement Clearinghouse.

“We need to stop the cash-out syndrome,” Williams said.

It doesn’t seem like companies should care whether a worker leaving a job decides to cash out the money they saved in a 401(k) plan, but studies have shown that people who don’t have enough saved for retirement wind up staying on the job longer and are more stressed about their finances, said Keith Overly, executive director for the state of Ohio Deferred Compensation plan.

Williams added that employers should be asking new hires whether they have a 401(k) from their old job and should try to help with the paperwork that goes into doing the transfer.

“We are all better off if there is not that kind of leakage,” Overly said. “Having a healthy [retirement balance] can be one of the most important benefits for an employee and an employer.”

About 14.8 million, or 22 percent, of active and contributing defined-contribution participants will change jobs each year, according to research from the Employee Benefit Research Institute. Of those job changers, Retirement Clearinghouse reports about 41 percent of these people will cash out of their 401(k).

“Someone with a $15,000 balance doesn’t want to do the work,” to roll the balance over to another retirement savings account, Williams said.

It was important for people to realize the problem, so to bring awareness, Retirement Clearinghouse created the National Retirement Savings Cash Out Clock. It is similar to the national debt clock that ticks away in New York City, but this one is online and focuses on year-to-date cash out and leakage rates from 401(k)s. By the end of 2017, it is expected to hit $68 billion.

If a worker decides to cash out, employers are required to keep 20 percent of the full amount to pay income tax. If the worker is under 59 ½ years old, they pay an extra 10 percent withdrawal penalty as well. According to American Century Investments Cash Out Calculator, a 29-year-old cashing out a $25,000 account would walk away with $18,000. Had they kept it in a 401(k) returning about 7 percent a year on investments, the calculator shows that money would grow to $285,599 at age 65.

“This can be a big problem for people,” Overly said. Retirement plans “aren’t supposed to be used like bank accounts.”

Surprisingly, only 37 percent of cash outs were for economic emergencies, according to a 2015 survey by Boston Research Technologies. Williams added that often people cash out simply because it was the easier route for the person at the time.

“The best choices are not always the easiest choices,” he said.

Overly said participants in his plan need to talk to management when cashing out. That provides an opportunity to make sure the person is aware of what they are doing.

“In some cases there may be some valid reasons, but your retirement plan should be your last resort,” Overly said.

Williams suggested companies should make it easier for new employees to roll over accounts from their old job to their new one. Retirement Clearinghouse is working with the Labor Department to make 401(k) plans automatically portable to a new employer. This way, 401(k) accounts would automatically follow a worker to a new job and get rolled into that company’s plan.

For the most part, rollovers are allowed today, but the process isn’t automatic or easy. In addition, it normally requires a good bit of paperwork for the participant, Williams said.

“By law, it is portable but in practice, people are left to do this on their own. This has lead to a severe amount of cash outs,” Williams said. “We’re never going to stop all of this, but implementing a program to help employees bring the money with them should help.”

Patty Kujawa is a writer in the Milwaukee area. Comment below or email editors@workforce.com.

I recently had an eye-opening generational experience while at a Slovenian picnic a few weeks ago. The crowd was varied (made up of the Slovenians who had immigrated to Chicago in the early 20th century and their descendants): 80-something-year-old immigrants who sit on picnic benches the whole time and have long conversations in their Eastern European tongue, 50-somethings playing bocce ball with a beer in hand and the 20-somethings like me.

The people in my parents’ generation undoubtedly talk about work or when they can finally retire. Where should they invest? Will retirement be in 10 or 15 years? Will they retire in Arizona or Texas or Asia? They speak like they’re one of those persnickety couples on House Hunters International, saying things like, “I really don’t care where we live as long as we’re five minutes from the beach,” and “But we could get a much better deal if we’re willing to move further from the beach!”

The people in my grandparents’ generation also bring up work and retirement, like when my grandfather shows off his construction union retirement gift (a gold watch that’s probably fake, he points out) and tells stories about his job.

Meanwhile, my similarly aged cousins and I have different thoughts on the same topic. Like on the evening news, my cousin and I both had a minor panic attacks when the anchor said something along the lines of, “College graduates today may not be able to retire until age 75.” That’s a big jump from 65. I’m hoping that’s a case of exaggeration for the sake of ratings.

In any case, it hit me that despite this huge generational divide between my parents and grandparents, we care about the same thing: security. The only difference is, we’re in very, very different places.

Much like my large, extended family, the workforce is multigenerational. That can seem daunting to a company managing employees in five different generations, but it’s less daunting when you consider that ultimately most people want the same thing. They’re just in different places in their lives in terms of attaining it.

Acclaris’ Carlos Hernandez

“Millennials don’t necessarily look at benefits in a wildly different way than the other generations. They’re worried about base pay, bonuses, retirement,” said Carlos Hernandez, vice president of strategic alliances at Acclaris, an information technology and services provider that manages health care plans. As an employer, “you have to offer the basics.”

Where there may be a difference, though, is the messaging itself, added Hernandez, who has more than 25 years of experience in the health care industry advising employers on how to best meet their benefits goals. Companies, when considering benefits offerings, have to use different messaging to different groups — like age groups — to show the value points they have. But it’s still the same program underneath that skin.

One way to facilitate the access to information, for example, is bring a financial firm to a lunch and learn every month and let employees sign up to speak to an adviser, Hernandez noted. This could be appealing to a baby boomer who’s retiring in 15 years, or someone just starting out their career who wants to get on the right path.

Also useful to facilitate access is a creating a touchpoint, like a mobile app or portal or private conference room, he added. Companies could use something like this to deliver services and guidance in private.

Finally, in terms of managing a multigenerational workforce, he suggested creating a committee or a strategic forum made up of employees of every generation. These representatives of the company could talk about issues, like financial or health benefits, from their own points of view.

“That sense of involvement cannot be understated,” he said.

Andie Burjek is a Workforce associate editor. Comment below, or email at aburjek@humancapitalmedia.com. Follow Workforce on Twitter at@workforcenews.

Our retirement is not our parents’ retirement. For many American employees in their generation, a good job meant access to a secure retirement income they could not outlive. Employers took center stage, assuming most of the financial risk of funding that retirement with employees largely removed from the process. Today, employers are far more likely to be facilitators of retirement saving, playing a critical supporting role while the employee is the star planner of the retirement show.

How did the idea that employers should offer secure retirement benefits through defined benefit plans, or pensions, evolve? How and why did this change over time to put more of the responsibility on employees to save through defined contribution plans such as 401(k)s? And how can benefits managers use new savings tools and employee benefits available today to help their employees retire smarter, happier and more financially secure?

The U.S. Retirement System

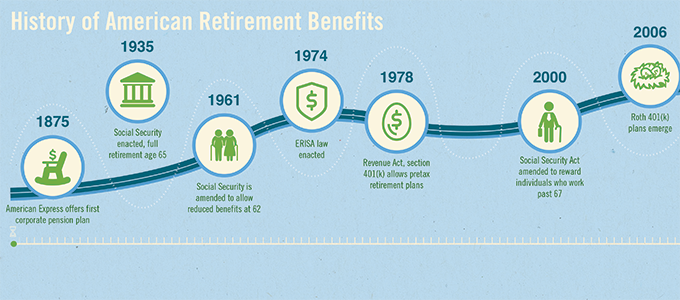

Retirement is a fairly modern concept with origins in military history. Until the late 1800s, those who had to work to earn their living worked their entire lives. Historians credit the Roman Empire with conceiving the idea of an income that continued after work service by offering pensions to retiring soldiers during the first century B.C. While this initiated a long tradition of military pensions, the concept of ceasing to work in later life didn’t begin to spread to the rest of the workforce until the 19th century.

Today, we think of a pension as a series of payments to be made to workers after the end of their working years. In the United States during the mid-1800s, a “pension” also referred to disability and survivor benefits. During the middle of that century, larger cities began to offer disability and retirement income benefits to police and firefighters. This trend expanded over time among public sector workers.

In 1875, The American Express Co. created the first private pension plan in the U.S. for the elderly and workers with disabilities. According to the Pension Research Council, by 1926 approximately 200 private pensions had been established by larger employers in the United States. Early pension benefits were designed to pay out a relatively low percentage of the employee’s pay at retirement and were not designed to replace the employee’s full final income.

The idea that employees should have some kind of a defined benefit in retirement gained traction during the boom decades that followed World War II. Large corporate employers took a paternal approach to their workers and offered pensions as part of their talent recruitment and retention efforts.

And it worked. It was not uncommon for workers to spend their entire careers at the same company back then. Compare that to 2014 when the U.S. Bureau of Labor Statistics reported the average employee tenure was 4.6 years.

Benefits grew richer over time, with many pension plans offering replacement incomes that covered more of the employees’ average pay. By 1970, 26.3 million private sector workers (45 percent of all private sector employees) were covered by some kind of pension plan. Participation held steady for several decades with 43 percent of private sector employees still covered by 1990.

With a traditional defined benefit plan, employees had little direct control over their retirement. To earn higher lifetime benefits in the plan, they could work longer, make a higher salary or live longer — but the employer controlled the contribution formula and the investments, and generally made all the contributions to fund the plan.

The ’70s brought America staggering inflation, disco, and legislation that changed retirement forever. In 1978, Congress passed The Revenue Act of 1978 in which Section 401(k) cleared the way for the establishment of defined contribution plans. The idea was revolutionary: Employees would be able to contribute their own money in a tax-advantaged way to an account to supplement any other retirement benefits they had with tax incentives for the employer to also contribute. The upshot? Over the past 38 years for the typical U.S. employee, the responsibility for developing a sustainable retirement income has shifted from the employer to the individual.

A “defined contribution plan” takes its name from the ability of the employee and/or employer to contribute a fixed sum to the plan. Over time, different types of plans evolved to serve different types of employees: 401(k) plans for private sector employees, 403(b) plans for nonprofit and public education employees, 457 plans for state and municipal employees and the Thrift Savings Plan for federal employees.

Today, the traditional pension is an endangered species. For the past decade, employers have been terminating defined benefit plans in record numbers and moving toward defined contribution plans. According to the Employee Benefits Research Institute, by 2011 69 percent of employee participants in a retirement plan at work were participating in a defined contribution plan, 24 percent were participating in both a defined contribution and a defined benefit plan, and just 7 percent were in a defined benefit plan only.

Sources: NelsonHall; 2015-16 HR Systems Survey, Sierra-Cedar; National Association of Professional Employer Organizations. Graphic courtesy of Financial Finesse.

Employees are Unprepared or Underprepared for Retirement

Employees are largely unprepared to shoulder the risk of saving adequately to fund retirement and making wise investment choices with those savings. According to the Financial Finesse 2015 Year in Review research on employee financial trends, only 22 percent of employees are confident that they are on track for retirement, even though 84 percent contribute to their retirement plan. (Editor’s note: The author is the CEO of Financial Finesse.)

When it comes to choosing appropriate investments in their retirement accounts, employees are also falling short. Only 46 percent of male employees and 36 percent of female employees are confident their investments are allocated appropriately in their retirement accounts. Problems with cash flow management and debt have a cascading effect on suppressing retirement savings rates.

Recent enhancements in retirement plan design, such as auto-enrollment and auto-escalation, are not enough to increase preparation. Employers must address cash management and overall financial wellness, educating them to better understand their role in retirement preparation and freeing up more funds for contributions toward their retirement goals. Integrating plan design enhancements with employee benefits education and communication can improve retirement preparedness.

Employers can increase the likelihood that employees will be better prepared for retirement by integrating retirement education into an overall financial wellness program that looks at cash flow, employee benefits and long-term financial goals. When in place, Financial Finesse’s research shows repeat users of workplace financial wellness benefits have shown a 88 percent improvement in the percentage of workers who are on track for retirement. Forward-thinking employers can take these six steps to improve employee retirement preparedness:

Increase the default deferral rate.

Automatically enroll employees in auto-escalation of their retirement savings.

Implement re-enrollment in the plan’s qualified default investment alternative, also known as a QDIA, an investment that may be used by retirement plan sponsors in the absence of direction from the plan participant.

Offer benefits planning to help employers understand and maximize the value of their benefits.

Enhance employee communications.

Develop a comprehensive financial wellness program.

More — and More Complex Benefits Choices

Employers and employees are also navigating major changes in health insurance benefits, including the move to high deductible health plans in conjunction with health savings accounts, which were created in 2003. Employees in general do not yet fully understand the advantages of HSAs in preparing for retirement, and employers have a high hurdle in helping them maximize this benefit.

Additionally, since the Roth individual retirement account was introduced in legislation sponsored by the late-Sen. William Roth Jr., R-Delaware, in 1997, Americans within certain income limits have been able to save after-tax contributions in an account that grows tax-free for retirement. The Roth 401(k), allowed by legislation passed in 2001, gave those employers who sponsor retirement plans the option to offer employees after-tax/tax-free distributions within the 401(k) structure. While slow to gain adoption, recently employees have been choosing Roth options in greater numbers.

Healthy Confusion

Employees generally remain confused over which health insurance and retirement plan options are best for their situation. They look to their employers to offer guidance on how to choose what’s right for them. Employers may consider offering targeted educational workshops or webcasts, print or email communications and personal financial coaching to help employees understand and maximize these benefits.

For health care, this includes ways to review the health coverage and out-of-pocket costs they have today, understand and compare plan options, decide which option is best for their unique situation and prepare for changes they’ll need to make in their cash management to take full advantage of the value of an HSA. Employers can also offer workers retirement plan education on the differences between pretax and after-tax contributions, and the general types of situations where one or the other makes sense.

The good news is that employers are well-positioned to help employees be the star planner of the retirement show so they can meet the challenges of improving retirement preparedness and make wise benefits decisions. According to a TIAA survey, 81 percent of respondents said they trust financial information from their employer. Financial Finesse’s 2015 Retirement Preparedness Research shows that the number of employees who say they are on track for retirement doubled with repeat usage of workplace financial wellness programs. While technology such as online financial education can play a supporting role, employers will gain the most influence and employee satisfaction with offering interaction with a financial coach who can help employees through the decision-making process.

Employers who offer support, guidance and education to assist employees in taking center stage throughout their careers in order to retire comfortably will have loyal, more financially confident employees. As reporter Emily Brandon said in “Pensionless: The 10-Step Solution for a Stress Free Retirement,” “Although you may never receive a pension from a former employer, you can do a lot to make the most of the retirement benefits you do have.”

With employers leading the way in prepping workers for the future, 21st century employees can still have a comfortable, secure retirement.

It seems like a lazy Sunday in The District, but I’m already pounding the keys on my laptop at the SHRM 2016 Annual Conference & Exposition. I even had my first interview with Jeff Tulloch, MetLife’s vice president of the PlanSmart, Workplace Benefits and Business Advantage group.

Since I have retirement on my mind with my latest “Last Word” column and Workforce’s upcoming July issue on retirement, I talked to Tulloch about what companies can do to help workers with retirement. An edited transcript follows.

Whatever Works: How do you get past the white noise that many employees hear when it comes to retirement planning?

Jeff Tulloch, MetLife

Jeff Tulloch: The first component is, where we are now compared to 10 years ago, people have woken up to, ‘OK, my parents maybe had a pension plan and they were taken care of, and, well, I don’t have that. So now, what do I do? How do I get myself secure?’ So I think there’s the stark reality that people now have. ‘I need to do something,’ but they don’t know where to go. ‘I see things in the paper, I see things in the magazines, I see things online, I talk to my friends.’ So getting past the white noise, we have this workshop [PlanSmart] offering that is a voluntary benefit. You come if you want. You’re not forced to go. And that gets people to take the first step forward. ‘I know I need information. I just don’t know what I need.’ And then once they get there, there’s a variety of information that’s provided to them that helps get them to a better spot. And then they can self-select if they want to take things to the next step, which is meeting with a financial adviser one on one. So it’s still difficult because, obviously, a large population is not financially well but that forum where — you’re not forced into it, you go if you want — and then you self-select how far you want to go with it helps get people [pointed] in the right direction.

WW: What mistakes are companies making in explaining retirement benefits?

Tulloch: I would say one would be thinking that the 401(k) plan is it. It’s the answer. And it’s not. The average balance nowadays is $100,000, maybe a little less than that. And that’s the average. A lot of people have a lot less. Probably one mistake is: ‘We put a lot of effort into our 401(k) plan, we did a great job of getting more people into it and contributing more, so we’ve done our job.’ And that’s just one component, one mistake. A second one kind of playing off that would be not realizing how stressed out people are regarding their financial matters and how that drains on the company’s productivity. ‘I’m on the phone with people trying to figure stuff out or I’m stressed out online looking stuff up, or I’m stressed out and therefore missing deadlines and not as productive as I should be.’ So I think those two things go together.

WW: Has the mentality changed on how employers approach employee retirement over the years?

Tulloch: I don’t know that I’d say it’s completely changed. I think [it’s] the reality of where companies are now financially and the challenge to be more and more competitive relative to who they are competing against. Companies [are] being stretched to figure out how to lower expenses. That’s the reality. The people we interact with, large corporations, they want to do what’s right. I think the same passion is generally there to help employees, but then there’s the reality of, ‘We can’t give you a pension plan anymore.’

WW: What about the smaller employers?

Tulloch: They are even more challenged just because of the resources available to them. And a small employer, if I’m the owner or one of the key managers, I’m so focused on the 14 jobs I have within the company that I’m stressed to figure out what to do for the employees. So that’s tough. There are tools out there to provide people with access to information, whether it’s online calculators or newsletters, things like that.

WW: What three bullet points do you have for companies to provide best practices to help employees with retirement planning?

Tulloch: The first would be drive a culture of helping support people financially from the top down. Make sure it’s not just something that an upper-level manager is supporting. Really start at the top, the CEO, the owner of the business, and really say, ‘This is important. We’re committed to it. We want our employees to be in a good spot, and we’re going to do everything we can.’

One would be start with the CEO on down. The second would be realize that there’s a commonality that most of us have some level of financial stress in our lives, but the range of what that stress is is extreme. You and I can be the same age and [have] the same income, but your stress might be that you’re trying to save for college. My stress might be I have a special-needs sibling that I’m taking care of. The third one might be I have no clue what I’m trying to save for retirement.

The second one would be realize there’s a wide need; it’s not just one answer.

The third would be accessibility. Do people want it on the phone, do they want a workshop setting, do they want it online on the intranet? And I think the answer is probably yes to all of that. So how can you deliver something that’s multimedia?

James Tehrani is Workforce’s managing editor. Follow Tehrani on Twitter at @WorkforceJames and like his blog on Facebook at “Whatever Works” blog.

To maintain my, ahem, lavish lifestyle, I’ll need to put away $2.2 million by the time I’m ready to retire at age 67, according to the retirement calculator on CNN Money. And with all those Social Security benefits promised to me, I’ll have it made.

As a longtime journalist and editor who torches fifty-dollar bills to light cigars, I scoff at this declaration about my retirement and any fearmongering from the financial experts out there, like this little rant on neglecting saving for retirement from Dave Ramsey: “You’re going to be so bad, you’re going to be ordering the cookbook ‘72 Ways to Prepare Alpo and Love It.’ ”

Well, that’s pretty ruff. I mean, rough.

“I could pawn my new Ferrari F60 for more than that,” I shout at my computer screen, adding a juicy raspberry and “na-na, na-na, boo-boo” for good measure.

Then reality hits.

Huh? Wait, I must have been daydreaming.

“Oh, crap,” I say to myself as I snap back to reality. There’s a better chance of Trump, Cruz, Clinton and Sanders singing “The hills are alive with the sound of music” together in a picturesque meadow than I being able to set aside more than $2 million to retire. Of course, my wife will have to fend for herself under this maddening retirement scenario. Love you, honey, but the “you” in CNN’s “Will you have enough to retire?” tool is second-person singular as far as I can tell, and there’s an “I” and a “me” in “retirement.” So …

But there is a ray of hope. If I hang on to my job until age 76, the calculator tells me I should be on track to have just enough money to retire. That is as long as I plan on being healthy for the rest of my days and I expire at age 92.

If I beat expectations and go for the century mark, or spend the last years of my life regretting those hot dogs and cheeseburgers I ate at backyard barbecues over the years, or those Bombay Sapphire martinis I imbibed at various social gatherings, or if my asthma catches up to me from the summers I spent breathing in smoke and coughing up black junk while grilling ribs at outdoor festivals, I could be hurting even more.

Medical bills: expensive. And playing bridge for money with people who are much better at cards than I am is expensive, too. Unfortunately, I’ve heard bad things about the “I’m gonna strike it rich” by playing the lottery every week strategy for retirement.

It’s not going to be easy for me to save enough for retirement for sure, but women have it even harder, writes Patty Kujawa in our retirement feature, “Making Up the Difference.” She cites a Transamerica report that found women are less likely than men to have access to a 401(k) and are also less likely to participate in one or even contribute to one.

Furthermore, in its 2016 Retirement Confidence survey, the Employee Benefits Research Institute found that 40 percent of unmarried women have less than $1,000 stashed away for retirement. Twenty-two percent of married women were under $1,000 as well.

The EBRI survey also offered this grim analysis: “Despite the fact that women tend to face higher expenses in retirement due to their greater longevity, unmarried women (36 percent) are more likely than their unmarried male counterparts (25 percent) to think they will need to accumulate less than $250,000 for retirement.”

Two hundred and fifty grand? What is this 1950?

If you had a quarter of a million dollars back then, it would be the same as almost $2.5 million today. Problem is it hasn’t been 1950 for, oh, 66 years.

Our friends at the Social Security Administration tell us that if you’re a female millennial born Jan. 1, 1982, you are expected to live almost 86 years, and if you make it to age 70, you’re on pace to live till 89.

That’s great, but we are going to start seeing more people work to 100 and beyond just to pay the bills.

It’s nice to know there are some organizations like Cedars-Sinai that offer a choice in retirement benefits. Employees at the Los Angeles-based health care facility can choose — yes, choose — between a defined contribution plan and a defined benefit plan.

While we can’t “turn back time to the good old days,” it’s important to know there are a lot of workers who are “stressed out” about retirement. Is there anything you, the HR community, can do to communicate differently about retirement? Clearly the scare tactics just aren’t working.

Let’s figure this out soon. I’m almost out of Alpo.

James Tehrani is Workforce’s managing editor. Follow Tehrani on Twitter at @WorkforceJames and like his blog on Facebook at “Whatever Works” blog.

“I plan to take it out as early as I can,” Beach said from her home in Arlington, Texas. “I don’t really know that much about Social Security, but I hear it’s going to go away.”

“I plan to take it out as early as I can,” Beach said from her home in Arlington, Texas. “I don’t really know that much about Social Security, but I hear it’s going to go away.”

Finally, the Pension Protection Act of 2006 allowed plan sponsors to automatically enroll workers into what is called a qualified default investment alternative, or QDIA, a type of investment that would meet a participant’s retirement needs. Target-date funds fall under that umbrella.

Finally, the Pension Protection Act of 2006 allowed plan sponsors to automatically enroll workers into what is called a qualified default investment alternative, or QDIA, a type of investment that would meet a participant’s retirement needs. Target-date funds fall under that umbrella.