For PR firm Walker Sands Communications, that round, sometimes frosted dessert didn’t just pack a lot of cream — it packed a lot of punch as well.

Mike Santoro, president of Walker Sands, wanted to learn how news traveled across his company. He turned his head toward the regular internal employee newsletter, wondering if it was an effective communication tool.

“When you’re a small company, it’s easy to spread the word. You stand up in the middle of the floor and yell, ‘Attention!’ As we’ve grown, it’s definitely been more challenging,” Santoro said. “We wanted to do an actual experiment to find out how they [employees] behave.”

Then, he thought about that popular breakfast treat. Santoro said he thought to himself, “What can we do with doughnuts?”

Besides making Homer Simpson the happiest man in the world?

At 9 a.m. on a Friday, two different versions of the same e-newsletter went out. One read, “Donuts in the Conference Room” at the top; the second placed the same phrase toward the bottom. By 10:30 a.m., 91 percent of the newsletter’s recipients were aware of the information but in a way that interested Santoro. Nearly half of the employees in the conference room had heard about the pastries from a source other than the newsletter. Santoro learned that the office newsletter is only slightly better than word of mouth — and that word of mouth only travels so far.

Walker Sands’ recent study raises an interesting question about effective perks and benefits communication strategies, which can be just as tricky and sticky as the icing on that pastry. How can employers effectively spread the word?

“Today’s employee and the ways of communicating have changed,” Santoro said. “It used to be, you could do direct mail, face-to-face. You could do phone calls. Now, people are consuming information” through many different kinds of outlets.

“As much as you can, communicate with pictures and video,” Santoro said. “That’s really important to be able to tell that story.”

Social media sites, Santoro said, are great methods of doing just that.

“Our own employees tend to be younger people,” he said, “who tend to communicate across Snapchat, Facebook, Instagram.”

But just because the digital age provides more communication tools, Santoro said the traditional in-person meetings should not be overlooked.

“We have quarterly meetings; we have monthly town halls where we gather everyone in the company together and tell them: ‘This is what’s most important for the month.’ Then you have these other secondary mechanisms, like the newsletter and active social channel,” Santoro said.

But communicating those perks and benefits doesn’t always have to revolve around “Who’s bringing the doughnuts?” David Daskal has also seen some unique strategies as director of business development at The Jellyvision Lab Inc., a business that creates interactive software to help employees learn about workplace benefits.

“Being human means you also have the freedom to have a little fun,” Daskal said. “Engaging posters and fliers in the break room, a raffle for everyone who participates in a benefits webinar. We’ve even worked with HR teams who have dressed up in costumes to help promote open enrollment.”

Sarah Foster is an editorial intern at Workforce. Comment below or email at editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

Consider the following example. ABC Co. has a policy that states that an employee is entitled to a 12-week leave of absence for any medical reason, and thereafter the company cannot guarantee a job upon an employee’s ability to return to work. Does this policy pass muster under the Americans with Disabilities Act?

Opinions differ sharply on whether an employer can satisfy its obligations under the ADA by implementing a neutral leave of absence policy that caps a maximum allowable leave (for example, a policy that says, “Employees who do not return to work following a maximum of six months leave will be presumed to have resigned,” or “Employees will be entitled to a maximum of six months of unpaid medical leave in appropriate circumstances, and thereafter the company cannot hold the employee’s position open or guarantee a position to which the employee can return.”).

One opinion that is clear, though, is that of the EEOC. According to the commission, in its recently published guidance titled “Employer-Provided Leave and the Americans with Disabilities Act,” the answer is likely “no.” According to the EEOC, “the prevalence of employer policies that deny or unlawfully restrict the use of leave as a reasonable accommodation,” which the agency believes “serve as systemic barriers to the employment of workers with disabilities.”

In my experience, employers deny leaves because they are simply trying to do the best they can to balance the operational needs of their business against the medical needs of an employee. Sometimes the business wins. The EEOC is trying to level the playing field by making sure that employers consider leaves in all cases when appropriate.

The guidance is broken down into six key areas, which highlight various issues for employers to consider when employees need medical leaves of absence not covered by, or in addition to, the Family and Medical Leave Act.

Equal access to leave under an employer’s leave policy. Employers must provide employees with disabilities access to the same leaves of absence rules as employees without disabilities.

Granting leave as a reasonable accommodation. An employer must consider providing unpaid leave to an employee with a disability as a reasonable accommodation if the employee requires it, and so long as it does not create an undue hardship for the employer.

Leave and the interactive process generally. After an employee requests leave as a reasonable accommodation, the employer should promptly engage in an “interactive process” with the employee, a discussion that focuses on the reasons for the leave, whether it’s blocked or intermittent, and its expected duration, which may include confirming information from the employee’s health care provider.

Maximum leave policies. Policies that place a hard cap on an employee’s leave of absence, without consideration of modifications or extensions as reasonable accommodations, are unlawful under the ADA.

Return to work and reasonable accommodation (including reassignment). Avoid “100 percent healed” policies, which mandate that an employee must be fully recovered before returning to work. They are unlawful. Instead, consider reasonable accommodations that will enable an employee to return before 100 percent healed, which might include transfer to a vacant position.

Undue hardship. Depending on the duration and frequency of the leave and the effect on the employer’s business, the leave of absence might be an undue hardship that an employer need not offer. An open-ended, indefinite leave is always an undue hardship.

Employers need to be practical and tread very lightly around the issue of leaves of absences until the EEOC softens its position. The agency is aggressively pursuing businesses that enforce these neutral leave policies to the detriment of employees with disabilities. Unless you want to end up in the EEOC’s crosshairs, I recommend adopting the following “A-E-I-O-You” approach to employee medical leaves:

Avoid leave policies that provide a per se maximum amount of leave.

Engage in the interactive process with an employee who needs an extended leave of absence.

Involve your employment counsel to aid in the process of deciding when an extended leave crosses the line from a reasonable accommodation to an undue hardship.

Open your workplace to employees with disabilities to demonstrate to the EEOC, if necessary, that you take your ADA obligations seriously.

You should document all costs associated with any extended unpaid leaves to help make your undue hardship argument, if needed.

Remembering “A-E-I-O-You” will help you avoid the defense of a costly disability discrimination lawsuit.

Jon Hyman is a partner at Meyers, Roman, Friedberg & Lewis in Cleveland. To comment, email editors@workforce.com. Follow Hyman’s blog at Workforce.com/PracticalEmployer.

Workplace deaths and injuries are on the rise, having reached their highest levels since 2008, despite dramatic improvements in worker-safety practices over the past few decades.

According to a recent study by the National Safety Council, a nonprofit organization that promotes health and safety, 4,132 workers died of unintentional injuries in the workplace in 2014, up 6 percent from the previous year, reflecting the largest spike in 20 years, according to safety expert John Dony.

“Forty years ago, we had lots of people dying from doing very dangerous work, but we realized that we need to put people in harnesses when they’re working on tall buildings, and we need to develop a system for reporting accidents,” said Dony, director of the Campbell Institute, the research arm of the National Safety Council. “We still have a good story to tell around workplace safety in the United States, but the fact that we’ve had a long history of maturity and improvement and yet we are seeing an increase in deaths and injuries is troubling.”

According to the council’s report, which is based on federal data, certain industries have seen a sharper rise in unintentional injuries such as falls, motor vehicle accidents, machinery accidents and exposure to harmful substances.

For employers, this can mean higher workers’ compensation costs and more indirect consequences like lost productivity, higher training costs to replace injured workers, lower employee morale and greater absenteeism. According to a 2016 study by the Liberty Mutual Research Institute for Safety, U.S. businesses spend about $1 billion a week in workers’ compensation costs for the worst occupational injuries. These include overexertion because of lifting, pulling or throwing, falling, being struck by an object and roadway accidents.

Older workers are being killed or injured in greater numbers.

According to the U.S. Bureau of Labor Statistics, there were 1,691 fatalities among workers 55 and older — a 4 percent increase over 2013. A recent report by Washington state’s department of labor found that more than half of workplace deaths in 2015 involved people over 50.

An aging workforce is likely one factor contributing to the increase in workplace deaths and injuries, Dony said, adding that it’s not clear if physical limitations associated with aging are to blame.

Whatever the reasons, employers need to do a better job of making their workplaces safer, he said.

Rita Pyrillis is a writer based in the Chicago area. Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

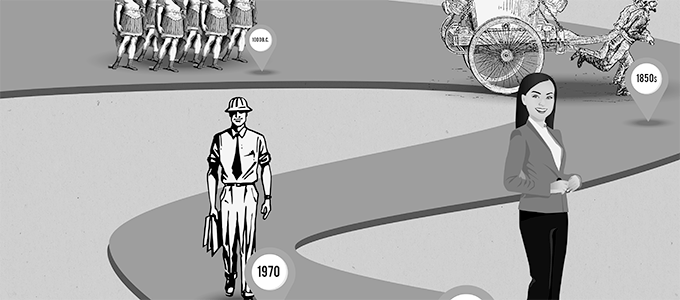

Our retirement is not our parents’ retirement. For many American employees in their generation, a good job meant access to a secure retirement income they could not outlive. Employers took center stage, assuming most of the financial risk of funding that retirement with employees largely removed from the process. Today, employers are far more likely to be facilitators of retirement saving, playing a critical supporting role while the employee is the star planner of the retirement show.

How did the idea that employers should offer secure retirement benefits through defined benefit plans, or pensions, evolve? How and why did this change over time to put more of the responsibility on employees to save through defined contribution plans such as 401(k)s? And how can benefits managers use new savings tools and employee benefits available today to help their employees retire smarter, happier and more financially secure?

The U.S. Retirement System

Retirement is a fairly modern concept with origins in military history. Until the late 1800s, those who had to work to earn their living worked their entire lives. Historians credit the Roman Empire with conceiving the idea of an income that continued after work service by offering pensions to retiring soldiers during the first century B.C. While this initiated a long tradition of military pensions, the concept of ceasing to work in later life didn’t begin to spread to the rest of the workforce until the 19th century.

Today, we think of a pension as a series of payments to be made to workers after the end of their working years. In the United States during the mid-1800s, a “pension” also referred to disability and survivor benefits. During the middle of that century, larger cities began to offer disability and retirement income benefits to police and firefighters. This trend expanded over time among public sector workers.

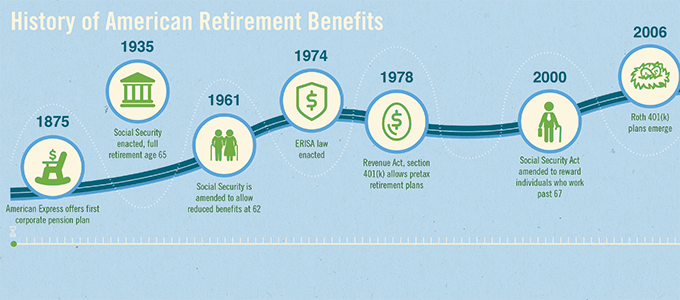

In 1875, The American Express Co. created the first private pension plan in the U.S. for the elderly and workers with disabilities. According to the Pension Research Council, by 1926 approximately 200 private pensions had been established by larger employers in the United States. Early pension benefits were designed to pay out a relatively low percentage of the employee’s pay at retirement and were not designed to replace the employee’s full final income.

The idea that employees should have some kind of a defined benefit in retirement gained traction during the boom decades that followed World War II. Large corporate employers took a paternal approach to their workers and offered pensions as part of their talent recruitment and retention efforts.

And it worked. It was not uncommon for workers to spend their entire careers at the same company back then. Compare that to 2014 when the U.S. Bureau of Labor Statistics reported the average employee tenure was 4.6 years.

Benefits grew richer over time, with many pension plans offering replacement incomes that covered more of the employees’ average pay. By 1970, 26.3 million private sector workers (45 percent of all private sector employees) were covered by some kind of pension plan. Participation held steady for several decades with 43 percent of private sector employees still covered by 1990.

With a traditional defined benefit plan, employees had little direct control over their retirement. To earn higher lifetime benefits in the plan, they could work longer, make a higher salary or live longer — but the employer controlled the contribution formula and the investments, and generally made all the contributions to fund the plan.

The ’70s brought America staggering inflation, disco, and legislation that changed retirement forever. In 1978, Congress passed The Revenue Act of 1978 in which Section 401(k) cleared the way for the establishment of defined contribution plans. The idea was revolutionary: Employees would be able to contribute their own money in a tax-advantaged way to an account to supplement any other retirement benefits they had with tax incentives for the employer to also contribute. The upshot? Over the past 38 years for the typical U.S. employee, the responsibility for developing a sustainable retirement income has shifted from the employer to the individual.

A “defined contribution plan” takes its name from the ability of the employee and/or employer to contribute a fixed sum to the plan. Over time, different types of plans evolved to serve different types of employees: 401(k) plans for private sector employees, 403(b) plans for nonprofit and public education employees, 457 plans for state and municipal employees and the Thrift Savings Plan for federal employees.

Today, the traditional pension is an endangered species. For the past decade, employers have been terminating defined benefit plans in record numbers and moving toward defined contribution plans. According to the Employee Benefits Research Institute, by 2011 69 percent of employee participants in a retirement plan at work were participating in a defined contribution plan, 24 percent were participating in both a defined contribution and a defined benefit plan, and just 7 percent were in a defined benefit plan only.

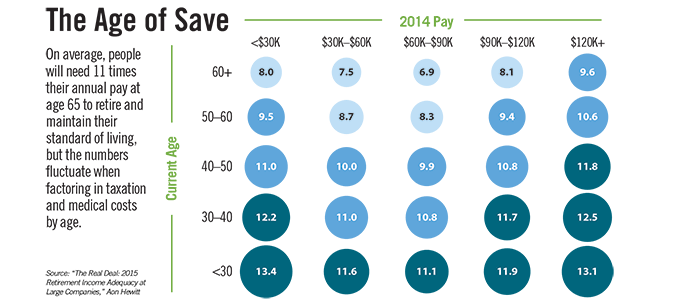

Sources: NelsonHall; 2015-16 HR Systems Survey, Sierra-Cedar; National Association of Professional Employer Organizations. Graphic courtesy of Financial Finesse.

Employees are Unprepared or Underprepared for Retirement

Employees are largely unprepared to shoulder the risk of saving adequately to fund retirement and making wise investment choices with those savings. According to the Financial Finesse 2015 Year in Review research on employee financial trends, only 22 percent of employees are confident that they are on track for retirement, even though 84 percent contribute to their retirement plan. (Editor’s note: The author is the CEO of Financial Finesse.)

When it comes to choosing appropriate investments in their retirement accounts, employees are also falling short. Only 46 percent of male employees and 36 percent of female employees are confident their investments are allocated appropriately in their retirement accounts. Problems with cash flow management and debt have a cascading effect on suppressing retirement savings rates.

Recent enhancements in retirement plan design, such as auto-enrollment and auto-escalation, are not enough to increase preparation. Employers must address cash management and overall financial wellness, educating them to better understand their role in retirement preparation and freeing up more funds for contributions toward their retirement goals. Integrating plan design enhancements with employee benefits education and communication can improve retirement preparedness.

Employers can increase the likelihood that employees will be better prepared for retirement by integrating retirement education into an overall financial wellness program that looks at cash flow, employee benefits and long-term financial goals. When in place, Financial Finesse’s research shows repeat users of workplace financial wellness benefits have shown a 88 percent improvement in the percentage of workers who are on track for retirement. Forward-thinking employers can take these six steps to improve employee retirement preparedness:

Increase the default deferral rate.

Automatically enroll employees in auto-escalation of their retirement savings.

Implement re-enrollment in the plan’s qualified default investment alternative, also known as a QDIA, an investment that may be used by retirement plan sponsors in the absence of direction from the plan participant.

Offer benefits planning to help employers understand and maximize the value of their benefits.

Enhance employee communications.

Develop a comprehensive financial wellness program.

More — and More Complex Benefits Choices

Employers and employees are also navigating major changes in health insurance benefits, including the move to high deductible health plans in conjunction with health savings accounts, which were created in 2003. Employees in general do not yet fully understand the advantages of HSAs in preparing for retirement, and employers have a high hurdle in helping them maximize this benefit.

Additionally, since the Roth individual retirement account was introduced in legislation sponsored by the late-Sen. William Roth Jr., R-Delaware, in 1997, Americans within certain income limits have been able to save after-tax contributions in an account that grows tax-free for retirement. The Roth 401(k), allowed by legislation passed in 2001, gave those employers who sponsor retirement plans the option to offer employees after-tax/tax-free distributions within the 401(k) structure. While slow to gain adoption, recently employees have been choosing Roth options in greater numbers.

Healthy Confusion

Employees generally remain confused over which health insurance and retirement plan options are best for their situation. They look to their employers to offer guidance on how to choose what’s right for them. Employers may consider offering targeted educational workshops or webcasts, print or email communications and personal financial coaching to help employees understand and maximize these benefits.

For health care, this includes ways to review the health coverage and out-of-pocket costs they have today, understand and compare plan options, decide which option is best for their unique situation and prepare for changes they’ll need to make in their cash management to take full advantage of the value of an HSA. Employers can also offer workers retirement plan education on the differences between pretax and after-tax contributions, and the general types of situations where one or the other makes sense.

The good news is that employers are well-positioned to help employees be the star planner of the retirement show so they can meet the challenges of improving retirement preparedness and make wise benefits decisions. According to a TIAA survey, 81 percent of respondents said they trust financial information from their employer. Financial Finesse’s 2015 Retirement Preparedness Research shows that the number of employees who say they are on track for retirement doubled with repeat usage of workplace financial wellness programs. While technology such as online financial education can play a supporting role, employers will gain the most influence and employee satisfaction with offering interaction with a financial coach who can help employees through the decision-making process.

Employers who offer support, guidance and education to assist employees in taking center stage throughout their careers in order to retire comfortably will have loyal, more financially confident employees. As reporter Emily Brandon said in “Pensionless: The 10-Step Solution for a Stress Free Retirement,” “Although you may never receive a pension from a former employer, you can do a lot to make the most of the retirement benefits you do have.”

With employers leading the way in prepping workers for the future, 21st century employees can still have a comfortable, secure retirement.

It seems like a lazy Sunday in The District, but I’m already pounding the keys on my laptop at the SHRM 2016 Annual Conference & Exposition. I even had my first interview with Jeff Tulloch, MetLife’s vice president of the PlanSmart, Workplace Benefits and Business Advantage group.

Since I have retirement on my mind with my latest “Last Word” column and Workforce’s upcoming July issue on retirement, I talked to Tulloch about what companies can do to help workers with retirement. An edited transcript follows.

Whatever Works: How do you get past the white noise that many employees hear when it comes to retirement planning?

Jeff Tulloch, MetLife

Jeff Tulloch: The first component is, where we are now compared to 10 years ago, people have woken up to, ‘OK, my parents maybe had a pension plan and they were taken care of, and, well, I don’t have that. So now, what do I do? How do I get myself secure?’ So I think there’s the stark reality that people now have. ‘I need to do something,’ but they don’t know where to go. ‘I see things in the paper, I see things in the magazines, I see things online, I talk to my friends.’ So getting past the white noise, we have this workshop [PlanSmart] offering that is a voluntary benefit. You come if you want. You’re not forced to go. And that gets people to take the first step forward. ‘I know I need information. I just don’t know what I need.’ And then once they get there, there’s a variety of information that’s provided to them that helps get them to a better spot. And then they can self-select if they want to take things to the next step, which is meeting with a financial adviser one on one. So it’s still difficult because, obviously, a large population is not financially well but that forum where — you’re not forced into it, you go if you want — and then you self-select how far you want to go with it helps get people [pointed] in the right direction.

WW: What mistakes are companies making in explaining retirement benefits?

Tulloch: I would say one would be thinking that the 401(k) plan is it. It’s the answer. And it’s not. The average balance nowadays is $100,000, maybe a little less than that. And that’s the average. A lot of people have a lot less. Probably one mistake is: ‘We put a lot of effort into our 401(k) plan, we did a great job of getting more people into it and contributing more, so we’ve done our job.’ And that’s just one component, one mistake. A second one kind of playing off that would be not realizing how stressed out people are regarding their financial matters and how that drains on the company’s productivity. ‘I’m on the phone with people trying to figure stuff out or I’m stressed out online looking stuff up, or I’m stressed out and therefore missing deadlines and not as productive as I should be.’ So I think those two things go together.

WW: Has the mentality changed on how employers approach employee retirement over the years?

Tulloch: I don’t know that I’d say it’s completely changed. I think [it’s] the reality of where companies are now financially and the challenge to be more and more competitive relative to who they are competing against. Companies [are] being stretched to figure out how to lower expenses. That’s the reality. The people we interact with, large corporations, they want to do what’s right. I think the same passion is generally there to help employees, but then there’s the reality of, ‘We can’t give you a pension plan anymore.’

WW: What about the smaller employers?

Tulloch: They are even more challenged just because of the resources available to them. And a small employer, if I’m the owner or one of the key managers, I’m so focused on the 14 jobs I have within the company that I’m stressed to figure out what to do for the employees. So that’s tough. There are tools out there to provide people with access to information, whether it’s online calculators or newsletters, things like that.

WW: What three bullet points do you have for companies to provide best practices to help employees with retirement planning?

Tulloch: The first would be drive a culture of helping support people financially from the top down. Make sure it’s not just something that an upper-level manager is supporting. Really start at the top, the CEO, the owner of the business, and really say, ‘This is important. We’re committed to it. We want our employees to be in a good spot, and we’re going to do everything we can.’

One would be start with the CEO on down. The second would be realize that there’s a commonality that most of us have some level of financial stress in our lives, but the range of what that stress is is extreme. You and I can be the same age and [have] the same income, but your stress might be that you’re trying to save for college. My stress might be I have a special-needs sibling that I’m taking care of. The third one might be I have no clue what I’m trying to save for retirement.

The second one would be realize there’s a wide need; it’s not just one answer.

The third would be accessibility. Do people want it on the phone, do they want a workshop setting, do they want it online on the intranet? And I think the answer is probably yes to all of that. So how can you deliver something that’s multimedia?

James Tehrani is Workforce’s managing editor. Follow Tehrani on Twitter at @WorkforceJames and like his blog on Facebook at “Whatever Works” blog.

While legal campaigns targeting the rights of LGBT people seem to be mushrooming across the country, a growing number of employers are leading the way in supporting the rights of transgender people in the workplace.

From Target Corp.’s recent announcement about allowing transgender employees and customers to use the bathroom that matches their gender identity to companies like Facebook Inc., Kroger Co. and Visa Inc. offering coverage for gender reassignment surgery, more employers are looking for ways to attract and retain lesbian, gay, bisexual and transgender workers. Offering comprehensive insurance coverage of procedures and therapies related to sex reassignment is one way of doing that.

But what may seem like a dramatic shift is the result of a long and concerted effort by activists and large employers to make the workplace more welcoming to LGBT workers, according to Beck Bailey, deputy director of employee engagement at the Washington, D.C.-based foundation.

“There is a new public awareness of transgender folks with Laverne Cox and Caitlyn Jenner, but corporate America has been committed to and leading in the area of basic nondiscrimination protections for gender identity for 15 years,” he said.

The HRC index rates companies based on their LGBT anti-discrimination policies and practices, whether they offer health coverage for transgender individuals and domestic partner benefits, and other measures.

Despite a wave of anti-gay backlash sparked in part by last year’s U.S. Supreme Court ruling in favor of marriage equality, LGBT advocates at Chicago’s Rush University Medical Center found widespread support for their push to offer transgender inclusive health benefits. In January, Rush became the first hospital in Illinois to do so, covering mental health counseling, hormone therapy, surgery and all other treatments related to gender transitions. Last year, the city of Chicago began offering similar coverage.

“The winds were definitely in our favor,” said Christopher Nolan, manager of community benefit and population health and chair of Rush’s LGBTQ health committee. “The director of benefits was working with us and our general counsel is a sponsor, so we had legal in our corner as well. You need a champion to do something like this, and we had lots of support.”

Hospital administrators believe the decision will benefit not only employees, but also the hospital and patients as well, according to Drew Elizabeth McCormick, Rush’s associate general counsel.

Christopher Nolan

“We want to be a desirable place for people to work, and by being more diverse and inclusive, we’re better able to relate to and provide services to all sorts of patients,” she said. “The cost is so minimal and the cultural value of offering these benefits is so high that we felt very comfortable making this decision.”

HRC’s Bailey said that offering these benefits has little effect on overall employee health care costs because the number of transgender people in the workforce in so small.

“By all accounts, this is a rare condition, and everyone’s journey is different,” he said. “Not all transgender people use the medical treatments available to them, so the utilization rate is quite low.”

While employers have been supportive, getting insurance companies to offer coverage to transgender people was an uphill battle, according to Bailey. Today, denying coverage to people who identify as transgender is illegal under federal law.

“Historically, when we look at transgender inclusive health care, the insurance industry has had broad blanket control,” he said. “In some cases, the exclusions were so broadly stated that we would find a transgender woman seeking treatment for migraines having coverage denied because it was deemed related to her transexualism.”

The Affordable Care Act, which was passed in 2010, prohibits insurers and providers from discriminating against patients because of their gender identity.

Currently, 14 states and the District of Columbia have issued similar policies aimed at private insurers, according to Anand Kalra, health program manager at the Transgender Law Center in Oakland, California.

“This is an important time for people in HR to pay attention to these things and to make sure that they have fair and equal treatment when it comes to company health care policies,” he said. “People may not be aware that what’s in their insurance contract is unlawful. It’s important for HR to understand what constitutes discrimination.”

Rita Pyrillis is a writer based in the Chicago area. Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

As a society, we’re often in denial about retirement. While most of us envision a future full of leisurely, work-free days, many people have done little to prepare for it. Daily Starbucks runs and racing out to buy the latest iPhone have become second nature; retirement planning has taken a back seat to today’s must-have indulgences.

Life is expensive, and the reality is that most of our daily expenses aren’t going anywhere in retirement. In fact, some of our out-of-pocket costs, namely health care, can go up. According to research by Fidelity Investments, the average couple who retired in 2015 will need $245,000 to cover health care throughout their retirement — up from $220,000 in 2014.

The Fidelity report went on to say that nearly 75 percent of those surveyed were most concerned about being able to afford unexpected health care costs in retirement, yet only 22 percent had actually factored those costs into financial planning. The good news is that it’s never too late to start, and offering a health savings account, or HSA, can be a great way to help employees get on the right track to a healthy financial future.

This article is online bonus content for Workforce’s upcoming July feature on retirement benefits.

Breaking Down the HSA and the FSA

HSAs have traditionally been thought of as spending accounts — often confused with flexible spending accounts, or FSAs — and a way to use pretax dollars to cover everyday health care costs. While that is true, that is only one advantage of an HSA. Designed to be paired with a high-deductible health plan, or HDHP, HSAs allow employees to set aside pretax dollars to cover their deductible, copayments and/or other expenses not covered by insurance.

But HSAs are more than just spending accounts. Here’s where they stand apart: There is no requirement for your employees to use the money they contribute in the current year — or even within the next five years. With no “use it or lose it” policy, the HSA stays with your employees wherever they go, even if they change jobs or health care plans. As long as they have an HSA-qualified health plan and no other impermissible coverage, they can continue to build savings that they can access as needed today, tomorrow and in retirement.

Thinking Beyond the 401(k)

Maybe you’re thinking, “That sounds like a 401(k), and we already offer those.” That’s terrific, and by all means, keep encouraging your employees to contribute to those plans, especially if your company matches contributions. However, with health care costs poised to eat into a big chunk of your employees’ retirement savings, it makes sense to also offer and encourage enrollment in an HSA to help them cover those expenses and protect their retirement income.

For example, in 2016, an employee with family coverage in an HSA-qualified health plan can contribute up to $6,750 to an HSA. Health care expenses are likely to arise during the year, and copayments or big-ticket items may fluctuate based on needs, like braces or new glasses, and the pretax dollars in an HSA can cover that. Because they are pretax, your employees’ money is going to go much further and can save workers an average of 30 percent on health care expenses. Any leftover funds at the end of the year stays in the HSA, accruing interest and growing year over year.

Taking Advantage of Triple Tax

HSA funds also have three distinct tax advantages:

The money that your employees contribute to their HSA goes in tax-free.

Their HSA balance accrues interest and grows tax-free.

Unlike a 401(k), when your employees are ready to use the money, the funds can be withdrawn tax-free as long as they are used for eligible health care expenses.

Similar to a 401(k), your employees also have the option of investing all or a portion of their HSA funds once they reach a minimum account balance. This can help increase their health care nest egg even more. The amount your employees are able to contribute is obviously dictated by their disposable income, but contributing as much as possible is ideal, given the triple tax advantage.

The neat part about socking away money is that, as your employees’ HSA balances start to grow and they better understand the financial power that comes with tax-free savings, the more they’ll likely want to be active participants, seeking opportunities to maximize their savings. If you support your HSA offering with targeted communications and educational resources, you can help empower your employees to take full advantage of their retirement and health care savings.

No matter their age, income or current retirement savings, an HSA can be a great savings option for your employees. Your employees’ physical and financial health is too important not to investigate the advantages of including an HSA in your benefits package. Acting now will help your employees better protect themselves and their families today and in the future.

Jody Dietel is the chief compliance officer at WageWorks Inc. Comment below or email editors@workforce.com. Follow Workforce on Twitter at @workforcenews.

You get what you pay for.” This adage rings especially true in the business world. Low salaries generally attract mediocre talent. Cheap technology is often inefficient and can require costly repairs. And free employee assistance programs can incur high health care costs for employers.

The current EAP usage rate across the industry is 6.9 percent, according to the Chestnut Global Partners’ 2016 EAP industry trends report. With so few employees using a practically free service — the typical employer allots just 1 percent of its health care budget to EAP services — it seems counterintuitive that EAPs would cost employers a lot in the long run.

The cost of providing access to an EAP has dropped in recent years, but unfortunately so has the quality of the programs being provided, according to Kent Sharkey, president and CEO of Ulliance Inc., a Troy, Michigan-based human resources consultancy.

When Sharkey started his company 26 years ago, the average per-employee-per-month fee for an EAP was $2.50. In order to stay competitive after the financial crisis of 2008, EAP providers have dropped that fee below a dollar, Sharkey said. Unfortunately, lower prices can often mean poorer services.

EAPs were originally developed to provide assessment and services for addressing a variety of personal problems and concerns that interfere with employees’ well-being and work performance. Interventions for issues such as depression and substance abuse were delivered in person, by telephone or over the Internet by licensed counselors. EAPs typically offered employees up to six of these sessions, said Dave Sharar, chief clinical officer at Chestnut.

The problem, Sharkey said, is that many of today’s free EAPs operate on an assess-and-refer model. Employees call the EAP phone number provided by their employer, but instead of receiving traditional telephonic counseling, they are referred to a long-term treatment provider outside of the EAP. This triggers a claim on the employer health care plan.

And given the rising cost of health care to both employers and employees, the last thing either party wants is to trigger more claims.

“If you’re experience-rated — meaning every year your insurance company looks at the health care costs — then your premiums will go up or down based on utilization,” Sharkey said. “If your EAP is merely directing more traffic to your health care plan, then it’s costing you and your employees a ton in the long run.”

The solution is for employers to increase their level of engagement with the EAP, according to Matt Mollenhauer, managing director at Chestnut.

“I would suggest to an employer that what they really need to do is dig deep into EAPs and ask questions,” Mollenhauer said. “They may be falling way short of what they thought they had purchased. There needs to be employer investment in the product they are buying.”

Know Why They’re Going

The first thing every employer should do in regard to managing their EAPs better is look at the usage rates, Mollenhauer said.

“The sense we’re getting from our book of business and EAP colleagues is that utilization of the EAP is on the rise compared to the past,” he said. “But that’s just the outer layer. The larger issue is that there seems to be more stress in the workplace, and the severity of cases appears to be on the increase.”

According to Chestnut’s 2016 report, stress-related issues were the top reason employees in North America accessed an EAP in 2015, accounting for 21 percent of EAP usage in that region.

While the increase in usage could be because of employers’ efforts to increase awareness of their EAP offerings, it’s the increase in severity that’s troublesome to Mollenhauer and Sharar.

“Employees are trying not to use their health care benefits because of the expense,” Mollenhauer said. “They are going to the EAP first. Stress within workplaces, either economic or work-related stress, is causing employees to a little ‘white-knuckling’ where they’re waiting too long to seek support.”

Providers such as Chestnut are seeing a response directly from employees that they need more than the standard six sessions to resolve their issues, Sharar added.

“More people are using their EAP because there’s no deductible or copay for it,” Sharar said. “Employees want to use it as much as they can.”

Free, or embedded EAPs as they are also known, are not flexible and typically don’t allow employers to make model changes midyear. Employers who are looking to be responsive to employee needs must stay on top of usage patterns and invest in standalone models that allow faster response times, Sharar said.

“Employers who are engaged with the EAP often invest in a ‘high touch’ program where they see the EAP integrated with an overall benefits strategy,” Sharar said. “When you understand how your employees use their benefits, you can ask for flexibility to meet those needs in a way that incurs the lowest possible costs.”

Get HR Involved

Even though EAPs are designed as a confidential service for employees, that doesn’t mean that a company’s human resources department shouldn’t be actively engaged with the EAP provider. Providers with HR and account management services are able to intervene before problems escalate., Sharkey said.

According to Ulliance’s book of business from 2015, performance issues ranked as the No. 3 issue among employees, behind substance abuse and anger management, respectively.

“We work with human resources to intervene with employees who have a personal problem that has developed into a performance problem,” Sharkey said. “We help employees get back on track before they seek medical help through the health insurance plan for issues including anxiety and depression.”

Developing a relationship in which HR personnel can directly refer employees to the EAP prevents a problem from festering, Mollenhauer added.

EAPs have also proven useful in dealing with a growing issue for HR managers: marijuana usage among employees. While it’s legal is some states, marijuana remains illegal on a federal level. The conflict creates problems for employers with offices in several states that currently have a zero-tolerance drug policy, Sharkey said.

“In response to employer feedback, we developed a program through which we provide random drug testing,” Sharkey said. “It gives employers an alternative to either terminating or tolerating an employee who has marijuana in their system. An employee who tests positive is formally referred to the EAP and undergoes random drug testing and counseling.”

Unlike employer-sponsored drug rehab programs, EAP-provided services require the employee to release their personal information so that the employer knows whether the employee is attending counseling and passing drug tests, Sharkey said.

In addition, the counseling occurs face to face, which has proven to be a more effective method of delivery.

Don’t Let Technology Become a Distraction

Like seemingly everything else in the workplace, technology is entering the EAP field with the promise of offering on-demand access to needed counseling services.

“The intent behind it is to create better-enhanced access for millennials and younger workers that are far more technology-driven,” Mollenhauer said.

Online counseling completed through synchronous or asynchronous emails and secure video conferences where counselor and client interact over a computer or mobile device are the first steps into implementing technology to modernize the offering, Chestnut’s Sharar said.

Sharkey thinks it’s an especially good outlet for millennials who are comfortable interacting on more of a digital platform, but he still believes in the tried-and-true method of face-to-face counseling.

“I believe it’s a great first step for people who are reaching out to the EAP, but there’s nothing like meeting face to face and developing a rapport with your EAP counselor and coach,” Sharkey said. “A lot of research and counseling suggests that the most important factor is the relationship between counselor and client.”

The American Psychological Association conducted a study in 2002 that found 31 percent of respondents reported an improved mental state after telephonic counseling compared with 54 percent with those who received face-to-face counseling.

Sharar worries that an attempt by employers to save on costs might be hurting employees in the long run.

“People with more serious issues may think that they’re getting things addressed with a telephone call or online chat when they actually have a more serious issue with a substance-abuse problem or marital issue that is not being dealt with,” Sharar said. “EAPs need to be careful of when technology is being used as a supplement vs. when it becomes a replacement.”

There is also a clear distinction between the type of technology being used. Mollenhauer is comfortable with the telephone and videoconferencing that have typically been used, but is more leery of the use of apps.

“Tracking mood and looking up marital tips on an app has a flashy appeal, but as fancy as all of those are and as engaging as they are in the short run, there is little research to suggest their long-term sustainability or that they are even clinically valid,” Mollenhauer said.

At the end of the day, there is clear value in the direct interaction provided by going in to see a counselor. Sharkey compares his counselors with coaches who observe employee behavior and are able to offer suggestions and support after developing a rapport with an employee client.

“We use a solutions-focused counseling model,” Sharkey said. “Sometimes people aren’t aware that what they are doing is harmful. We do an assessment and develop a personal action plan that includes assigning homework throughout the week. An hour of counseling doesn’t change things. It’s when you apply it in the real world and see what actually works that makes a difference. In a counseling office, it’s always easier than when you talk to your significant other about a problem. You have to be agile, and face-to-face counseling allows that.”

While high-tech apps and videoconferences over cellphones could increase usage rates, Sharar warns against using “clicks” as a measure of an EAP’s effectiveness.

“We tend to get caught up on high utilization has the most important metric,” Sharar said. “But high utilization doesn’t speak to specific results or what happened with those people who used the service. Website clicks and phone calls don’t directly lead to an outcome.”

Return on investment calculates an investment purely on financial terms, Sharar said. The EAP is so inexpensive to begin with that employers should focus on getting fewer, more effective outcomes than trying to see how many employees they can cycle through.

“I hope we’re moving back into a trend where employers very consciously engage with the EAP as a valued business partner,” Mollenhauer said. “In the times of cost-cutting, employers have gone with free and I’m hoping that trend will reverse and employers will see that there is no value proposition in those ‘free’ programs. EAPs need to evolve to the point where they’re being integrated to help solve employee performance and resiliency issues.”

One of my biggest fears as a journalist – other than not getting the facts straight – is that no one is reading what I write.

If your immediate response is, “Check the number of Facebook likes, duh,” I challenge you to remember the last article you “liked” that you actually read all the way through. I don’t want to be “liked.” I want to write articles that readers engage with, articles that make them think and at the very least leave them a little better informed.

That’s why I love it when readers write back. Good or bad, I get a great sense of satisfaction out of knowing that what I’ve written triggered enough emotion in another person that they felt compelled to let me know how they’re feeling.

This very situation happened a few months ago with a story I wrote for the January issue of Workforce titled, “Caring for the Caregiver.” It was about employees who care for their aging or ill parents in addition to holding down a full time job. It’s no small task, and 15 percent of the U.S. workforce is currently trying to do it. The intention was to shine light on an underreported issue and to give employers ideas on how to support these employees.

Based on the Facebook likes, it was well received.

But then I got a letter from Laura Francis, the director of marketing at River software. With patience and gratitude she informed me that while accurate, my story was too narrow in its scope.

“I really appreciated your article on caring for caregivers,” Francis wrote. “It’s an incredibly important topic we need to address in society. Unfortunately, I feel like you overlooked a huge piece of this caregiver puzzle: parents of children with special needs.”

Her note struck a chord with me. I hadn’t even considered parents of special-needs children. Worse, none of the experts I spoke with for the story brought it up, either. I did some research, and according to the U.S. Census Bureau Report, one in every 26 families reported having a child with a disability. That’s a huge number of working adults. And it immediately made me wonder what, if anything, employers are doing to help ease that burden.

So I gave Francis a call, and she graciously shared her story.

Francis is the mother of a 6-year-old son who has cerebral palsy, epilepsy and cortical visual impairment in addition to other special needs. He can’t sit up on his own. He can’t crawl. He can’t walk. He can’t talk. He can’t feed himself. He needs someone with him all the time. Francis is that someone.

She considers herself lucky, though. Working for a small company like River has been a blessing.

“They know my family,” Francis said. “I’m not just some faceless name on a list. I’ve been with the company for 16 years so they’ve been with me through all of this. They are so responsive and flexible and I think flexibility is the key for parents of special-needs children.”

Francis works from home so that both she and her husband can care for their son. But River’s contribution goes beyond that. Last year when the company was switching insurance providers they called Francis first and asked her to make sure all her doctors would still be in network. They didn’t want to make a move that would leave her son uncovered.

“They are very thoughtful and respectful and open hearted and kind,” Francis said.

The Affordable Care Act also has been a blessing for Francis and parents like her. Before the legislation was passed in 2010, Francis had a $1 million lifetime maximum benefit for her health insurance policy. GIven her son’s medical needs, they had almost spent more than half of that. The ACA eliminated lifetime maximumsand made it so insurance companies can no longer deny coverage based on preexisting conditions.

“WIth all of the health issues my son faces, we would surely have faced this problem had there not been a law in effect to protect us,” Francis said.

While Francis is grateful for all that River and government legislation have done for her, she understands that not all parents of special-needs children have an ideal working situation. Her advice to those parents and their employers is to encourage conversation and understanding.

“One of the most important things for me is having my co-workers understand that caring for a special-needs child takes a lot out of you,” Francis said. “It can be exhausting. If you come to work one day and you’re just not on your game they can understand why without making assumptions about your commitment to the job.”

For employers considering treating parents of special-needs children the same way they treat parents who are responsible for elderly family members, here’s Francis’ advice: Don’t.

“These situations might feel similar, but they can be quite unique,” Francis said. “A lot of that is why it’s easy for us to get overlooked in the grand scheme of things. We’re trying to do our jobs and keep the family running. There’s not a lot of energy left to advocate for ourselves. Having benefits and ways to communicate within the workplace is so helpful.”

So for all the employers out there reading this, don’t make my mistake. Create a welcoming environment for all employees so that those with challenges like Francis feel comfortable coming to you knowing adjustments can be made so they can take care of work and family – without compromise.

At Workforce, we’ve covered many tough topics that are often viewed as taboo in the workplace such as mental illness, addiction and Alzheimer’s disease.

Discussions about these issues are difficult to have in any setting, but conversations at work about deeply personal struggles are fraught with concerns about privacy, legality, job security and other issues. There’s only so much that we want our employers to know about our lives and only so much that employers really want to know.

But some things must be openly addressed to create a supportive workplace where employees can do their best during tough times knowing that others care. One of those things is a topic that most of us want to avoid, even though none of us can — dying.

Those of us who have watched a loved one die know the blanket of pain and grief that covers us, making it hard to move through the day. Imagine carrying that heaviness to work where business goes on as usual.

Recently, I watched my cousin shuttle between her job, the hospital where her mother was admitted after a fall and, ultimately, to hospice. Her employer seemed supportive, but she had only so many paid days off at her disposal so she lived in an exhausting loop of home, work and hospice until her mother died weeks later.

I also watched a good friend juggle a demanding job and the care of her elderly parents — both in the hospital — while at the same time managing their financial and legal affairs.

While both my cousin and friend are talented and hard-working, I’m sure that they struggled to stay focused and present on the job. I don’t know what kind of support their workplaces offered, but it’s becoming clear that employers need to think more about how to help workers through the dying process, whether through programs like end-of-life planning or caregiver or survivor support services.

An aging workforce, medical advances that extend life and the growing ranks of caregivers means that more employees will be face to face with mortality, either their own or that of a loved one. Employers must be prepared to deal with this reality.

Struggling with end-of-life issues is a heavy emotional and often a financial burden for workers who are overwhelmed with grief, anger, fear and a host of other emotions that make it difficult to function. And that has a direct effect on productivity, performance, absenteeism and the cost of employee benefits.

According to Dr. J. Brent Pawlecki, chief health officer at Goodyear Rubber & Tire Co., employers are not doing enough to help their workers through these tough times.

“By making it a priority, employers can address the end of life as a specific workforce management challenge and work to understand the full impact on their employees,” he wrote in a 2010 article published in the journal Health Affairs.

He advised employers to develop tools to facilitate discussions around end-of-life issues, offering help in completing advanced directives and resources to assist with funeral arrangements and estate settlement issues. He also suggests offering a plan with a carrier that covers end-of-life counseling.

Many of these things are starting to happen.

In 2014, Goodyear partnered with The Conversation Project to distribute 2,400 toolkits to guide employees in having end-of-life discussions. The organization was co-founded by journalist Ellen Goodman and the Institute for Healthcare Improvement to facilitate discussions around dying. The National Business Group on Health also offers similar support to employers. Pitney Bowes and General Electric are other companies that offer support services in this area.

This year, Medicare began paying doctors to have end-of-life discussions with their patients, and a growing number of insurers like Blue Cross Blue Shield of Massachusetts are offering end-of-life benefits to encourage patients and providers to talk about death and to increase services that can help the dying live out their remaining days with dignity.

Thankfully, the “death panel” hysteria that erupted during debates over the Affordable Care Act years ago is behind us and a more thoughtful approach to the difficult business of dying is underway.

It’s in the best interests of employers to help usher it along.

It all started with a doughnut.

It all started with a doughnut.